Show R Code

set.seed(123)

e <- rnorm(100, mean = 0, sd = 1)

ggAcf(e, lag.max = 20) +

labs(title = "ACF — White Noise") +

theme_ts()

The ARIMA (AutoRegressive Integrated Moving Average) model is one of the most widely used statistical methods for time series forecasting. The Box-Jenkins methodology — developed by George Box and Gwilym Jenkins — provides a systematic four-stage approach for identifying, estimating, validating, and applying ARIMA models.

Four basic model types are involved:

| Model | Acronym | Description |

|---|---|---|

| Autoregressive | AR | Current value depends on its own past values |

| Moving Average | MA | Current value depends on past error terms |

| Mixed Autoregressive and Moving Average | ARMA | Combination of AR and MA |

| Mixed Autoregressive Integrated Moving Average | ARIMA | ARMA applied to differenced series |

A \(p\)th-order autoregressive model, AR(\(p\)), is:

\[ y_t = \phi_0 + \phi_1 y_{t-1} + \phi_2 y_{t-2} + \cdots + \phi_p y_{t-p} + \varepsilon_t \tag{1} \]

where:

Using the backward shift operator \(B\), Equation (1) becomes:

\[ (1 - \phi_1 B - \phi_2 B^2 - \cdots - \phi_p B^p)\,y_t = \phi_0 + \varepsilon_t \]

\[ y_t = \phi_0 + \phi_1 y_{t-1} + \varepsilon_t \tag{2} \]

\[ \Rightarrow (1 - \phi_1 B)\,y_t = \phi_0 + \varepsilon_t \tag{3} \]

The current value at time \(t\) equals the mean plus a contribution from one period back, plus the error term.

A \(q\)th-order moving average model, MA(\(q\)), is:

\[ y_t = \phi_0 + \varepsilon_t + \theta_1 \varepsilon_{t-1} + \theta_2 \varepsilon_{t-2} + \cdots + \theta_q \varepsilon_{t-q} \tag{4} \]

where:

In backshift notation:

\[ y_t = \phi_0 + (1 + \theta_1 B + \theta_2 B^2 + \cdots + \theta_q B^q)\,\varepsilon_t \]

\[ y_t = \phi_0 + \theta_1 \varepsilon_{t-1} + \varepsilon_t \tag{5} \]

\[ \Rightarrow y_t = \phi_0 + (1 + \theta_1 B)\,\varepsilon_t \]

ARMA(\(p,q\)) combines AR order \(p\) and MA order \(q\):

\[ y_t = \phi_0 + \phi_1 y_{t-1} + \cdots + \phi_p y_{t-p} + \varepsilon_t + \theta_1 \varepsilon_{t-1} + \cdots + \theta_q \varepsilon_{t-q} \tag{6} \]

In backshift notation:

\[ (1 - \phi_1 B - \cdots - \phi_p B^p)\,y_t = \phi_0 + (1 + \theta_1 B + \cdots + \theta_q B^q)\,\varepsilon_t \tag{7} \]

\[ y_t = \phi_0 + \phi_1 y_{t-1} + \theta_1 \varepsilon_{t-1} + \varepsilon_t \]

\[ \Rightarrow (1 - \phi_1 B)\,y_t = \phi_0 + (1 + \theta_1 B)\,\varepsilon_t \]

When the stationarity assumption is not fulfilled, the series must be differenced \(d\) times to achieve stationarity. The resulting model is ARIMA(\(p,d,q\)).

Let \(w_t = y_t - y_{t-1}\) (first difference, assumed stationary). Then:

\[ w_t = \phi_0 + \phi_1 w_{t-1} + \theta_1 \varepsilon_{t-1} + \varepsilon_t \tag{8} \]

\[ (1 - \phi_1 B)\,w_t = \phi_0 + (1 + \theta_1 B)\,\varepsilon_t \tag{9} \]

Setting \(\phi_0 = 0\) and substituting \(w_t = (1 - B)y_t\):

\[ (1 - \phi_1 B)(1 - B)\,y_t = (1 + \theta_1 B)\,\varepsilon_t \]

Expanding both sides:

\[ y_t - y_{t-1} - \phi_1 y_{t-1} + \phi_1 y_{t-2} = \varepsilon_t + \theta_1 \varepsilon_{t-1} \tag{10} \]

Solving for \(y_t\):

\[ y_t = (1 + \phi_1) y_{t-1} - \phi_1 y_{t-2} + \varepsilon_t + \theta_1 \varepsilon_{t-1} \tag{11} \]

Equation (11) resembles ARIMA(2,0,1), but it remains ARIMA(1,1,1) — the coefficients do not independently satisfy stationarity conditions for a second-order AR model.

Exercise: Write the backward shift operator formulations for:

For series exhibiting a seasonal component, seasonal differencing is required to remove the seasonality effect.

Let \(z_t\) be the seasonally differenced series:

\[ z_t = y_t - y_{t-12} \quad \text{(monthly)} \qquad z_t = y_t - y_{t-4} \quad \text{(quarterly)} \]

If \(z_t\) is still not stationary, apply regular differencing: \(w_t = z_t - z_{t-1}\).

General SARIMA notation: \(\text{SARIMA}(p,d,q)(P,D,Q)_s\)

| Parameter | Meaning |

|---|---|

| \(p\) | Non-seasonal AR order |

| \(d\) | Non-seasonal differencing order |

| \(q\) | Non-seasonal MA order |

| \(P\) | Seasonal AR order |

| \(D\) | Seasonal differencing order |

| \(Q\) | Seasonal MA order |

| \(s\) | Length of seasonal period |

Example: ARIMA\((1,1,1)(1,1,1)_{12}\): \(p=1\), \(d=1\), \(q=1\) (non-seasonal); \(P=1\), \(D=1\), \(Q=1\) (seasonal); \(s=12\) (monthly data).

Step 1 — Non-seasonal part ARIMA(1,1,2):

\[ (1 - \phi_1 B)(1 - B)(1 - B^4)\,y_t = (1 + \theta_1 B + \theta_2 B^2)\,\varepsilon_t \]

Step 2 — Seasonal part SARIMA(1,1,1):

\[ (1 - \Phi_1 B^4)(1 - B^4)\,y_t = (1 + \Theta_1 B^4)\,\varepsilon_t \]

Step 3 — Combined model:

\[ (1 - \phi_1 B)(1 - B)(1 - \Phi_1 B^4)(1 - B^4)\,y_t = (1 + \theta_1 B + \theta_2 B^2)(1 + \Theta_1 B^4)\,\varepsilon_t \]

Exercise: Write the backward shift operator formulations for:

The Box-Jenkins methodology involves four iterative stages:

| Stage | Name | Description |

|---|---|---|

| 1 | Model Identification | Use ACF/PACF and ADF test to determine \(p\), \(d\), \(q\) |

| 2 | Model Estimation | Estimate parameters using OLS or MLE |

| 3 | Model Validation | Check residuals for white noise (Ljung-Box, AIC, BIC) |

| 4 | Model Application | Generate forecasts from the best model |

If validation fails, return to Stage 1 and revise the model.

General identification rules:

The ACF measures the linear correlation between observations separated by lag \(k\):

\[ r_k = \frac{\text{Cov}(y_t,\, y_{t+k})}{\sqrt{\text{Var}(y_t)\,\text{Var}(y_{t+k})}} \tag{12} \]

At lag 1:

\[ r_1 = \frac{\text{Cov}(y_t,\, y_{t+1})}{\sqrt{\text{Var}(y_t)\,\text{Var}(y_{t+1})}} \tag{13} \]

Under stationarity, \(\text{Var}(y_t) = \text{Var}(y_{t-k}) = \sigma^2\), so:

\[ r_k = \frac{\text{Cov}(y_t,\, y_{t+k})}{\text{Var}(y_t)} \tag{14} \]

The approximate 95% confidence band for each ACF coefficient is:

\[ r_k \pm \frac{1.96}{\sqrt{T}} \tag{15} \]

For \(y_t = \phi_0 + \varepsilon_t\) with \(\varepsilon_t \overset{iid}{\sim} (0, \sigma_\varepsilon^2)\), setting \(\phi_0 = 0\):

At lag 0:

\[ r_0 = \frac{E(\varepsilon_t^2)}{\sigma_\varepsilon^2} = 1 \]

At lag \(k > 0\):

\[ r_k = \frac{E(\varepsilon_t\,\varepsilon_{t+k})}{\sigma_\varepsilon^2} = 0 \quad \text{(errors are independent)} \]

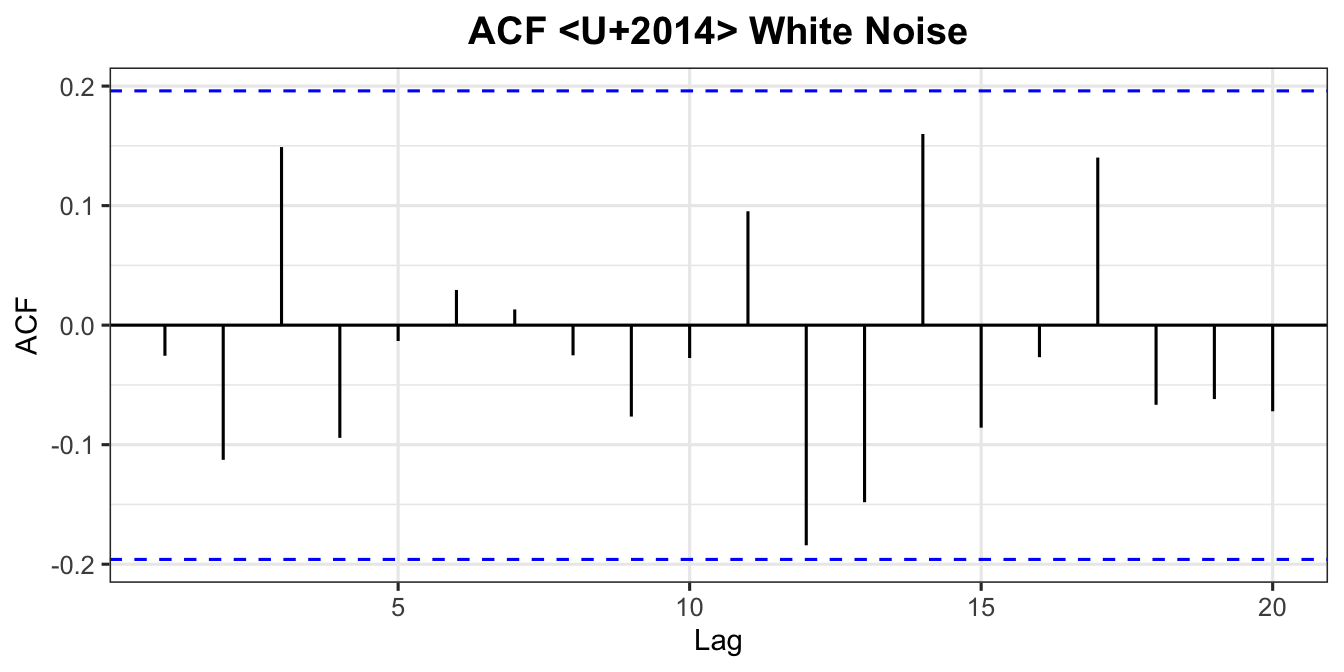

All autocorrelations at lags \(k > 0\) are zero. A white noise ACF shows all spikes within the confidence bounds.

set.seed(123)

e <- rnorm(100, mean = 0, sd = 1)

ggAcf(e, lag.max = 20) +

labs(title = "ACF — White Noise") +

theme_ts()From Chapter 4, for \(y_t = \phi_1 y_{t-1} + \varepsilon_t\) (with \(\phi_0 = 0\)):

Multiplying both sides by \(y_{t-k}\) and taking expectations:

\[ \gamma_1 = \phi_1\,\gamma_0 \implies r_1 = \phi_1 \]

In general, by the Yule-Walker equations:

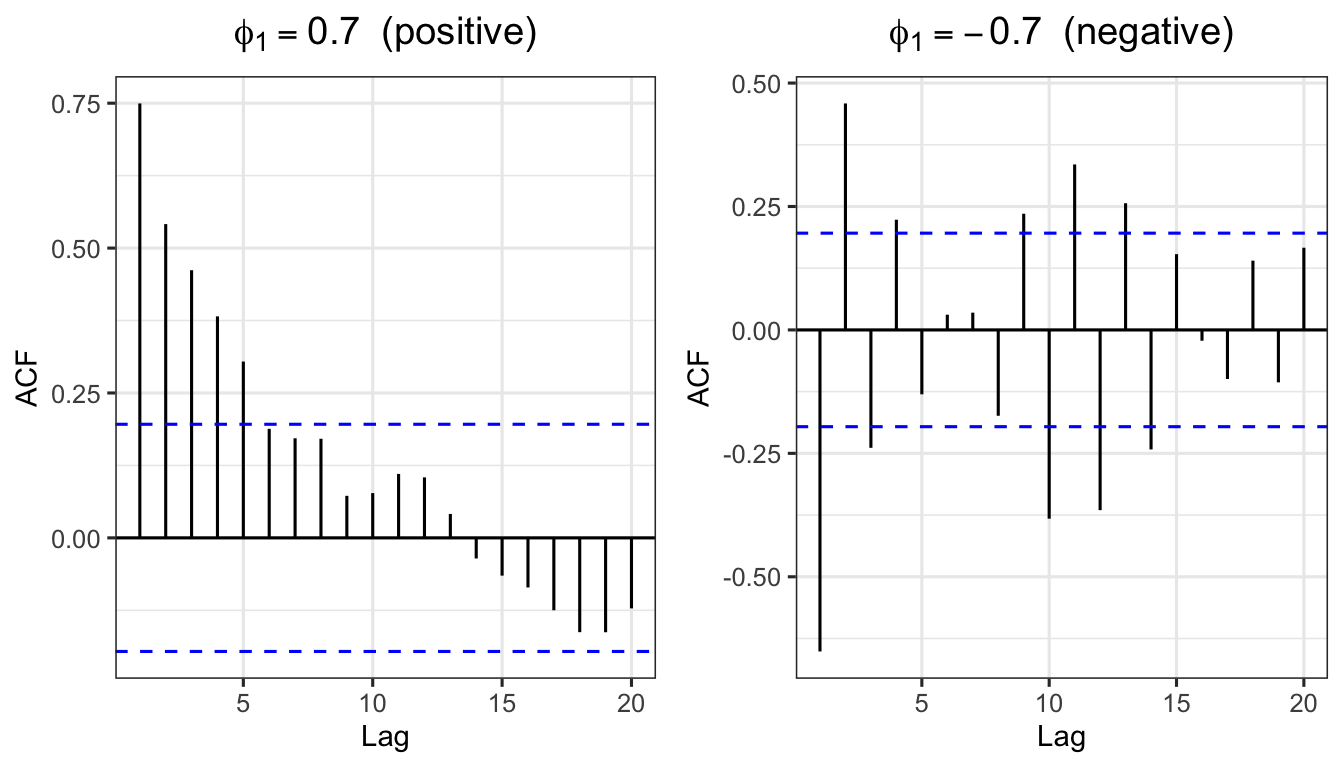

\[ \gamma_k = \phi_1^k\,\gamma_0 \implies r_k = \phi_1^k \tag{16} \]

Pattern:

set.seed(111)

ar1_pos <- arima.sim(model = list(order = c(1,0,0), ar = 0.7), n = 100)

ar1_neg <- arima.sim(model = list(order = c(1,0,0), ar = -0.7), n = 100)

p_pos <- ggAcf(ar1_pos, lag.max = 20) +

labs(title = expression(phi[1] == 0.7 ~ " (positive)")) + theme_ts()

p_neg <- ggAcf(ar1_neg, lag.max = 20) +

labs(title = expression(phi[1] == -0.7 ~ " (negative)")) + theme_ts()

grid.arrange(p_pos, p_neg, ncol = 2)

Example: For AR(1) with \(\phi_1 = 0.7\), theoretical ACF values:

\[r_1 = 0.7^1 = 0.700, \quad r_2 = 0.7^2 = 0.490, \quad r_3 = 0.7^3 = 0.343, \quad \ldots\]

Exercise for AR(2): For \(y_t = \phi_0 + \phi_1 y_{t-1} + \phi_2 y_{t-2} + \varepsilon_t\), prove that:

\[r_1 = \frac{\phi_1}{1 - \phi_2}, \qquad r_2 = \frac{\phi_1^2 + \phi_2(1+\phi_2)}{1-\phi_2}\]

For \(y_t = \phi_0 + \theta_1 \varepsilon_{t-1} + \varepsilon_t\):

\[ \text{Var}(y_t) = \gamma_0 = (1 + \theta_1^2)\,\sigma_\varepsilon^2 \]

\[ \gamma_1 = \theta_1\,\sigma_\varepsilon^2 \tag{17} \]

\[ \gamma_k = 0 \quad \text{for } k \geq 2 \]

Hence:

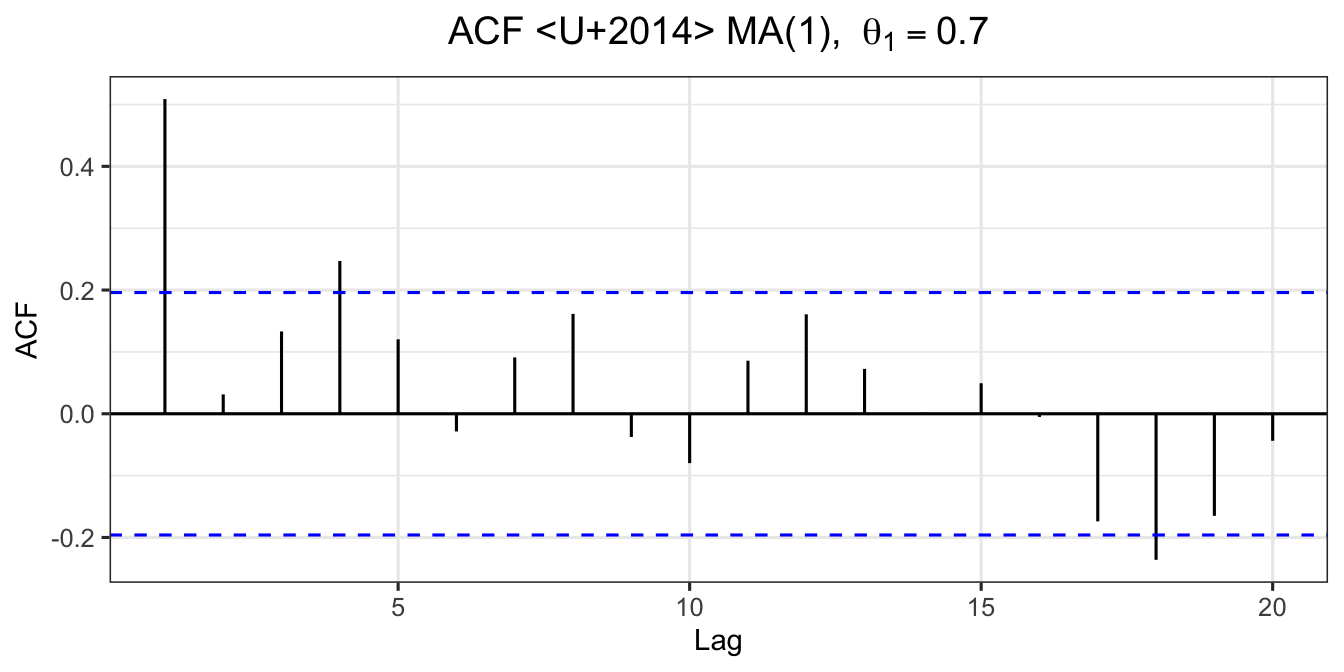

\[ r_1 = \frac{\theta_1}{1 + \theta_1^2}, \qquad r_k = 0 \text{ for } k \geq 2 \tag{18} \]

Pattern: ACF has exactly \(q\) significant spikes (cuts off after lag \(q\)).

Example: MA(1) with \(\theta_1 = 0.7\):

\[r_1 = \frac{0.7}{1 + 0.7^2} = \frac{0.7}{1.49} = 0.4698 \tag{19}\]

set.seed(111)

ma1 <- arima.sim(model = list(order = c(0,0,1), ma = 0.7), n = 100)

ggAcf(ma1, lag.max = 20) +

labs(title = expression("ACF — MA(1), " ~ theta[1] == 0.7)) +

theme_ts()

Exercise for MA(2): For \(y_t = \phi_0 + \theta_1\varepsilon_{t-1} + \theta_2\varepsilon_{t-2} + \varepsilon_t\), prove that:

\[r_1 = \frac{\theta_1 + \theta_1\theta_2}{1 + \theta_1^2 + \theta_2^2}, \qquad r_2 = \frac{\theta_2}{1 + \theta_1^2 + \theta_2^2}\]

The PACF measures the correlation between \(y_t\) and \(y_{t-k}\) after removing the linear effects of the intermediate lags \(y_{t-1}, y_{t-2}, \ldots, y_{t-k+1}\).

The PACF is computed iteratively via the Yule-Walker equations. The PACF at lag \(k\), denoted \(\alpha_k\), is:

\[ \alpha_k = \frac{r_k - \displaystyle\sum_{j=1}^{k-1} \phi_j^{(k-1)}\,r_{k-j}} {1 - \displaystyle\sum_{j=1}^{k-1} \phi_j^{(k-1)}\,r_j} \tag{20} \]

with the recursion \(\phi_j^{(k)} = \phi_j^{(k-1)} - \alpha_k\,\phi_{k-j}^{(k-1)}\).

| Model | ACF | PACF | Example |

|---|---|---|---|

| AR(\(p\)) | The coefficients show a decay pattern | There are \(k\) significant spike(s) | If the PACF shows that there is one significant spike observed at lag 1 and ACF exhibits a decay pattern, the suggested model is AR(1). |

| MA(\(q\)) | There are \(k\) significant spike(s) | The coefficients show a decay pattern | If the ACF shows that there is one significant spike observed at lag 1 and PACF exhibits a decay pattern, the suggested model is MA(1). |

| ARMA(\(p\),\(q\)) | There are \(k\) significant spike(s) | There are \(k\) significant spike(s) | If the ACF shows that there is one significant spike observed at lag 1 and PACF shows that there is one significant spike observed at lag 1, the suggested model is ARMA(1,1). |

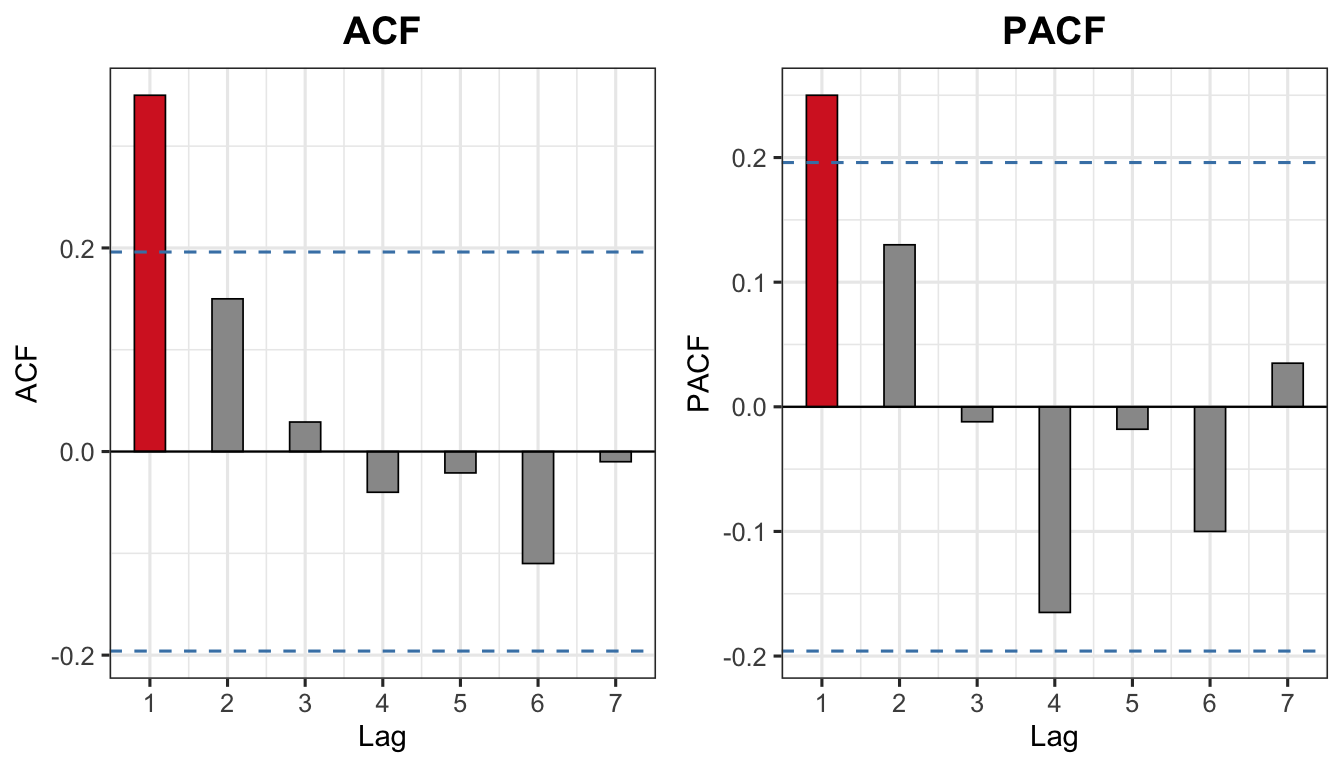

For a time series with \(T = 100\) observations, the sample ACF and PACF values at lags 1 to 7 are given as:

| Lag | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|

| ACF | 0.35 | 0.15 | 0.029 | −0.04 | −0.021 | −0.11 | −0.01 |

| PACF | 0.25 | 0.13 | −0.012 | −0.165 | −0.018 | −0.10 | 0.035 |

The 95% confidence band is:

\[\pm \frac{1.96}{\sqrt{T}} = \pm \frac{1.96}{\sqrt{100}} = \pm 0.196\]

Any spike that falls outside \(\pm 0.196\) is considered statistically significant.

T_obs <- 100

ci <- 1.96 / sqrt(T_obs) # ±0.196

lag_vals <- 1:7

acf_vals <- c(0.35, 0.15, 0.029, -0.04, -0.021, -0.11, -0.01)

pacf_vals <- c(0.25, 0.13, -0.012, -0.165, -0.018, -0.10, 0.035)

df_acf <- data.frame(lag = lag_vals, value = acf_vals,

sig = abs(acf_vals) > ci)

df_pacf <- data.frame(lag = lag_vals, value = pacf_vals,

sig = abs(pacf_vals) > ci)

p_acf_ex <- ggplot(df_acf, aes(x = lag, y = value, fill = sig)) +

geom_bar(stat = "identity", width = 0.4, colour = "black", linewidth = 0.3) +

geom_hline(yintercept = ci, linetype = "dashed", colour = "steelblue") +

geom_hline(yintercept = -ci, linetype = "dashed", colour = "steelblue") +

geom_hline(yintercept = 0, colour = "black", linewidth = 0.4) +

scale_fill_manual(values = c("TRUE" = "#d62728", "FALSE" = "grey60"),

guide = "none") +

scale_x_continuous(breaks = lag_vals) +

labs(title = "ACF", x = "Lag", y = "ACF") +

theme_ts()

p_pacf_ex <- ggplot(df_pacf, aes(x = lag, y = value, fill = sig)) +

geom_bar(stat = "identity", width = 0.4, colour = "black", linewidth = 0.3) +

geom_hline(yintercept = ci, linetype = "dashed", colour = "steelblue") +

geom_hline(yintercept = -ci, linetype = "dashed", colour = "steelblue") +

geom_hline(yintercept = 0, colour = "black", linewidth = 0.4) +

scale_fill_manual(values = c("TRUE" = "#d62728", "FALSE" = "grey60"),

guide = "none") +

scale_x_continuous(breaks = lag_vals) +

labs(title = "PACF", x = "Lag", y = "PACF") +

theme_ts()

grid.arrange(p_acf_ex, p_pacf_ex, ncol = 2)

Interpretation:

When both ACF and PACF show \(k\) significant spikes at the same lags, the series is best described by an ARMA model. Here \(k=1\) at lag 1, so ARMA(1,1) is the starting candidate.

set.seed(42)

sim_ar1 <- arima.sim(model = list(order=c(1,0,0), ar=0.7), n=200)

sim_ma1 <- arima.sim(model = list(order=c(0,0,1), ma=0.7), n=200)

sim_arma <- arima.sim(model = list(order=c(1,0,1), ar=0.7, ma=0.5), n=200)

p1 <- ggAcf(sim_ar1, lag.max=20) + labs(title="AR(1) — ACF") + theme_ts()

p2 <- ggPacf(sim_ar1, lag.max=20) + labs(title="AR(1) — PACF") + theme_ts()

p3 <- ggAcf(sim_ma1, lag.max=20) + labs(title="MA(1) — ACF") + theme_ts()

p4 <- ggPacf(sim_ma1, lag.max=20) + labs(title="MA(1) — PACF") + theme_ts()

p5 <- ggAcf(sim_arma, lag.max=20) + labs(title="ARMA(1,1) — ACF") + theme_ts()

p6 <- ggPacf(sim_arma, lag.max=20) + labs(title="ARMA(1,1) — PACF") + theme_ts()

grid.arrange(p1, p2, p3, p4, p5, p6, nrow=3)

We demonstrate the full four-stage Box-Jenkins procedure using S&P 500 E-mini Futures (ES=F) daily adjusted close prices, April–December 2025, downloaded directly from Yahoo Finance via the quantmod package.

autoplot(as.ts(est_snp)) +

labs(title = "S&P 500 Futures (ES=F) — Estimation Set",

subtitle = "Daily adjusted close price, Apr–Oct 2025",

x = "Observation", y = "Price (USD)") +

theme_ts()

p_acf_snp <- ggAcf(est_snp, lag.max = 30) +

labs(title = "ACF — SNP Level") + theme_ts()

p_pacf_snp <- ggPacf(est_snp, lag.max = 30) +

labs(title = "PACF — SNP Level") + theme_ts()

grid.arrange(p_acf_snp, p_pacf_snp, ncol = 2)

adf.test(est_snp)

Augmented Dickey-Fuller Test

data: est_snp

Dickey-Fuller = -2.857, Lag order = 5, p-value = 0.2192

alternative hypothesis: stationarySince \(p\)-value \(> 0.05\), we fail to reject \(H_0\) — the series is non-stationary.

diff_snp <- diff(est_snp)

autoplot(as.ts(diff_snp)) +

labs(title = "S&P 500 Futures — First Difference",

subtitle = "Daily price changes",

x = "Observation", y = expression(Delta ~ "Price")) +

theme_ts()

adf.test(na.omit(diff_snp))

Augmented Dickey-Fuller Test

data: na.omit(diff_snp)

Dickey-Fuller = -6.1097, Lag order = 5, p-value = 0.01

alternative hypothesis: stationarySince \(p\)-value \(\leq 0.05\), we reject \(H_0\) — the differenced series is stationary. Order of differencing: \(d = 1\).

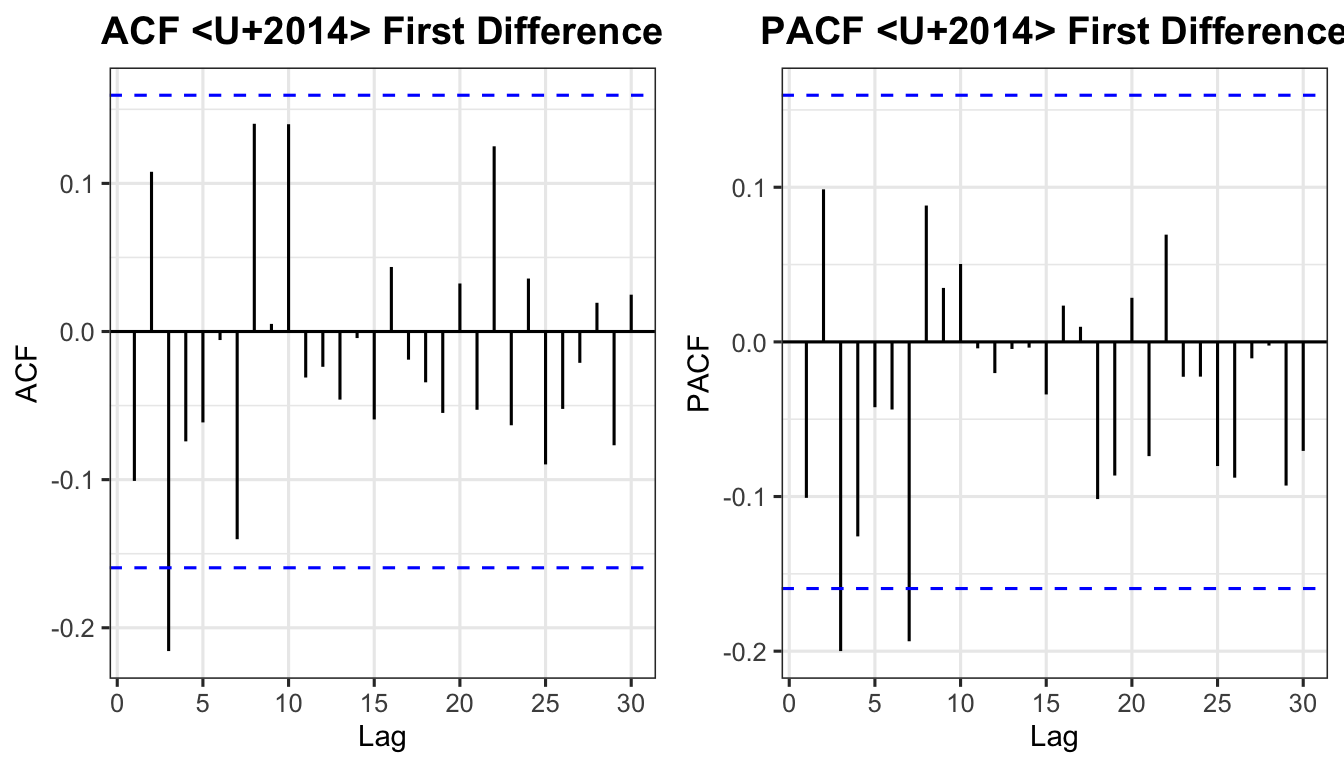

p_acf_d <- ggAcf(diff_snp, lag.max = 30, na.action = na.omit) +

labs(title = "ACF — First Difference") + theme_ts()

p_pacf_d <- ggPacf(diff_snp, lag.max = 30, na.action = na.omit) +

labs(title = "PACF — First Difference") + theme_ts()

grid.arrange(p_acf_d, p_pacf_d, ncol = 2)

Suggested model: ARIMA(2,1,1)

Competing models to compare: ARIMA(1,1,0) and ARIMA(2,1,2).

est_tbl <- as_tsibble(ts(as.numeric(est_snp)))

eva_tbl <- as_tsibble(ts(as.numeric(eva_snp)))

m211 <- est_tbl |> model(ARIMA(value ~ pdq(2,1,1)))

m110 <- est_tbl |> model(ARIMA(value ~ pdq(1,1,0)))

m212 <- est_tbl |> model(ARIMA(value ~ pdq(2,1,2)))

report(m211)Series: value

Model: ARIMA(2,1,1)

Coefficients:

ar1 ar2 ma1

0.6848 0.0219 -0.7805

s.e. 0.2093 0.0947 0.1924

sigma^2 estimated as 5408: log likelihood=-861.72

AIC=1731.45 AICc=1731.72 BIC=1743.52Estimated equation for ARIMA(2,1,1):

\[ (1 - \hat\phi_1 B - \hat\phi_2 B^2)(1 - B)\,y_t = (1 + \hat\theta_1 B)\,\varepsilon_t \tag{21} \]

Exercise: Write the estimated equations for ARIMA(1,1,0) and ARIMA(2,1,2) using the coefficient values from report().

The Ljung-Box statistic tests whether residuals are white noise:

\[ Q^*_{\text{calc}} = T(T+2)\sum_{k=1}^{h} \frac{r_k^2}{T-k} \tag{22} \]

approximately \(\chi^2\) with \((h - p - q)\) degrees of freedom.

If \(p\)-value \(> 0.05\) → fail to reject \(H_0\) → residuals are white noise → model is well-specified.

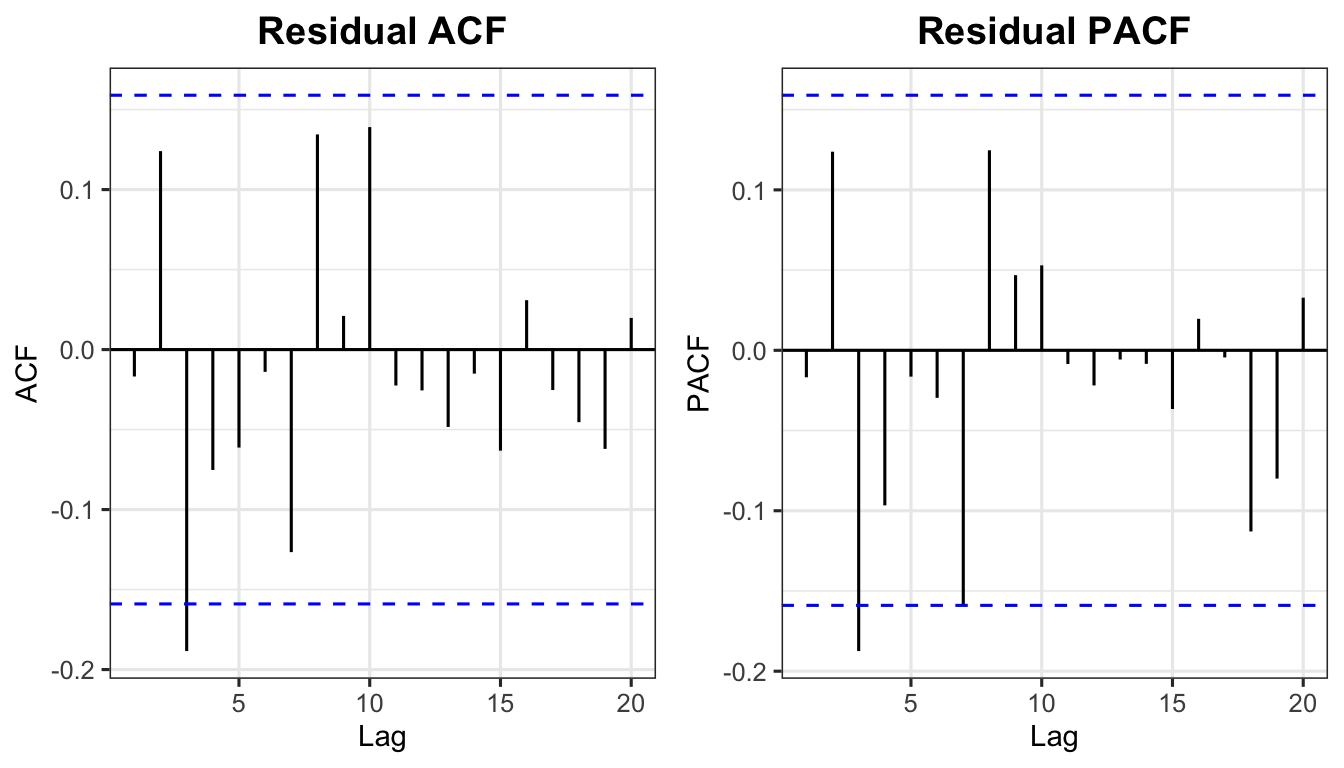

resid211 <- residuals(m211)

Box.test(resid211$.resid, lag = 20, type = "Ljung-Box", fitdf = 4)

Box-Ljung test

data: resid211$.resid

X-squared = 21.023, df = 16, p-value = 0.1776p_ra <- ggAcf(resid211$.resid, lag.max = 20, na.action = na.omit) +

labs(title = "Residual ACF") + theme_ts()

p_rpa <- ggPacf(resid211$.resid, lag.max = 20, na.action = na.omit) +

labs(title = "Residual PACF") + theme_ts()

grid.arrange(p_ra, p_rpa, ncol = 2)

Akaike’s Information Criterion (AIC):

\[ \text{AIC} = -2\log(L) + 2(p + q + k + 1) \tag{23} \]

where \(L\) is the likelihood, and \(k = 1\) if \(\phi_0 \neq 0\), else \(k = 0\).

Corrected AIC (AICc):

\[ \text{AICc} = \text{AIC} + \frac{2(p+q+k+1)(p+q+k+2)}{T - p - q - k - 2} \tag{24} \]

Bayesian Information Criterion (BIC):

\[ \text{BIC} = \text{AIC} + [\log(T) - 2](p + q + k + 1) \tag{25} \]

Lower AIC / AICc / BIC = better model. BIC penalises complexity more heavily than AIC.

bind_rows(

glance(m211) |> mutate(Model = "ARIMA(2,1,1)"),

glance(m110) |> mutate(Model = "ARIMA(1,1,0)"),

glance(m212) |> mutate(Model = "ARIMA(2,1,2)")

) |>

select(Model, AIC, AICc, BIC) |>

arrange(AIC)# A tibble: 3 x 4

Model AIC AICc BIC

<chr> <dbl> <dbl> <dbl>

1 ARIMA(2,1,2) 1725. 1725. 1743.

2 ARIMA(1,1,0) 1728. 1728. 1734.

3 ARIMA(2,1,1) 1731. 1732. 1744.The model with the lowest AIC/BIC is selected as the best model.

When two ARMA models produce the same series, they exhibit parameter redundancy. For example, a white noise process \(y_t = \varepsilon_t\) can be rewritten as:

\[ y_t = -0.5\,y_{t-1} + \varepsilon_t + 0.5\,\varepsilon_{t-1} \tag{26} \]

which superficially resembles ARMA(1,1) but is not a genuinely different model. Always inspect ACF/PACF diagnostics to avoid over-parameterisation.

Example: ARIMA(1,1,1) forecast derivation

Expanded equation (from Equation 11):

\[ y_t = (1 + \phi_1)\,y_{t-1} - \phi_1\,y_{t-2} + \varepsilon_t + \theta_1\,\varepsilon_{t-1} \tag{27} \]

One-step-ahead forecast (substitute \(t = T+1\), set \(\varepsilon_{T+1} = 0\)):

\[ \hat{y}_{T+1|T} = (1 + \hat\phi_1)\,y_T - \hat\phi_1\,y_{T-1} + \hat\theta_1\,\varepsilon_T \tag{28} \]

Two-step-ahead forecast (\(\varepsilon_{T+2} = \varepsilon_{T+1} = 0\), replace \(y_{T+1}\) with \(\hat{y}_{T+1|T}\)):

\[ \hat{y}_{T+2|T} = (1 + \hat\phi_1)\,\hat{y}_{T+1|T} - \hat\phi_1\,y_T \tag{29} \]

The process continues for all future periods \(h = 3, 4, \ldots\)

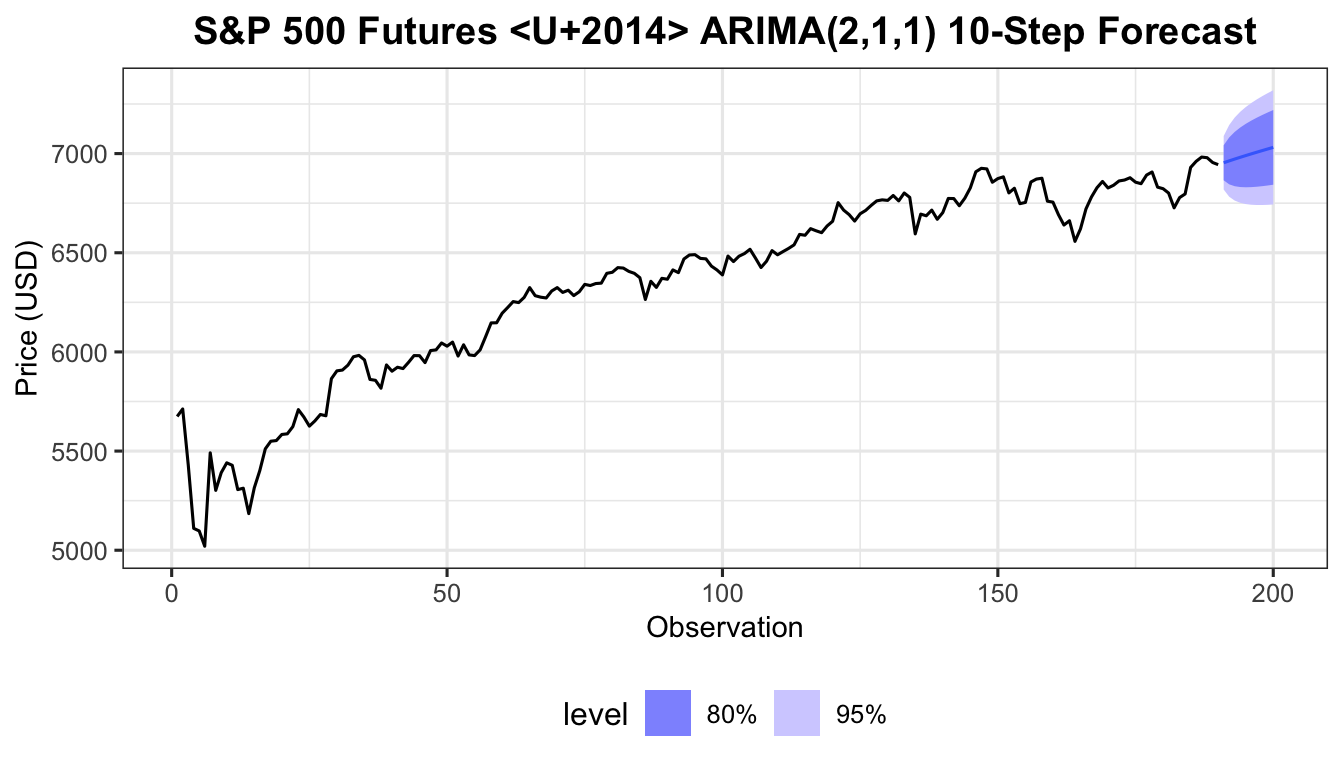

snp_tbl <- as_tsibble(ts(as.numeric(snp)))

m211_full <- snp_tbl |> model(ARIMA(value ~ pdq(2,1,1)))

m211_full |>

forecast(h = 10) |>

autoplot(snp_tbl, level = c(80, 95)) +

labs(title = "S&P 500 Futures — ARIMA(2,1,1) 10-Step Forecast",

x = "Observation", y = "Price (USD)") +

theme_ts()

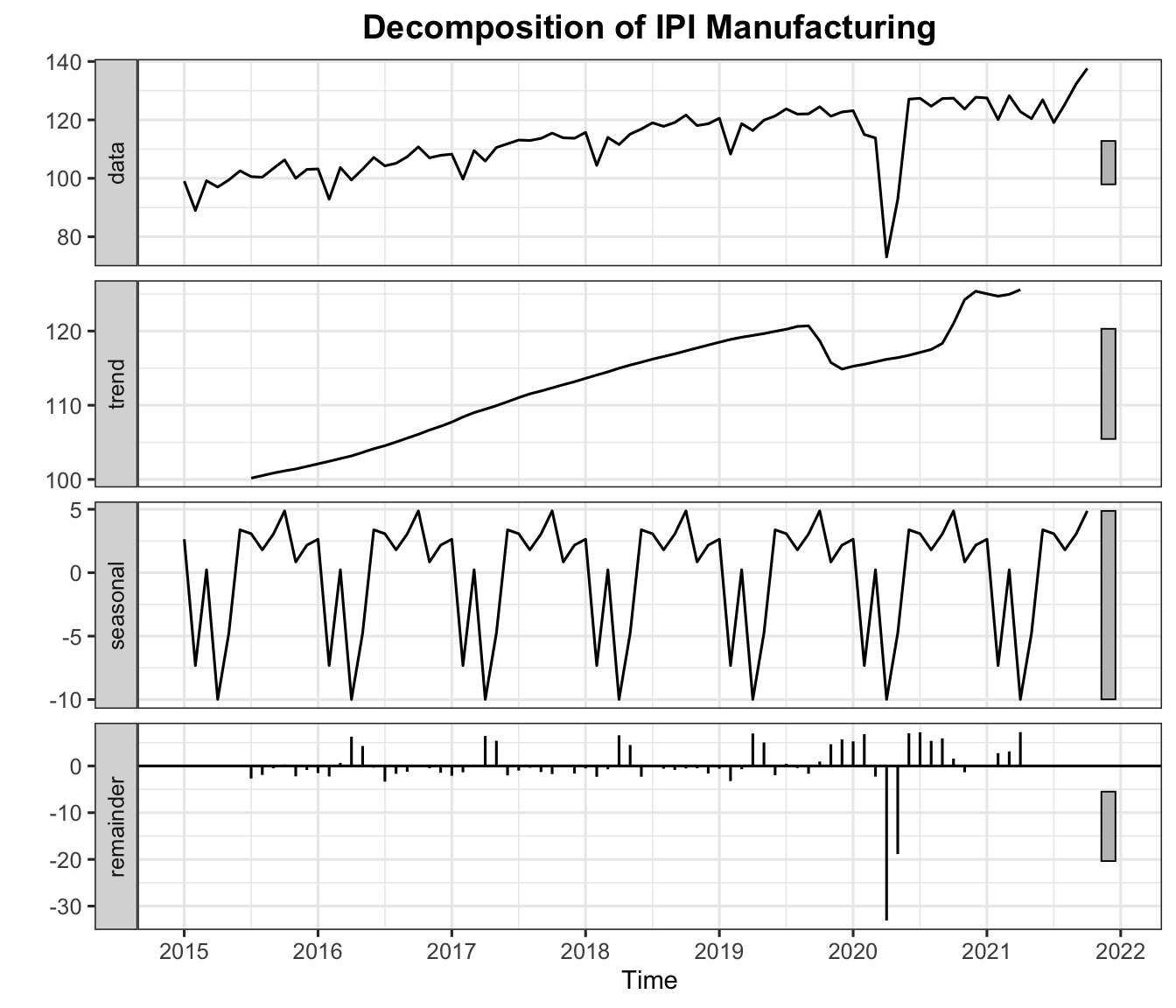

We now apply the full Box-Jenkins procedure to the Malaysia IPI Manufacturing Index (monthly, January 2015 to November 2025) — a series with both trend and seasonality.

The steps for SARIMA identification are:

# Estimation (first 82 obs) and evaluation (remaining) sets

n_total <- length(ipi_ts)

sest <- head(ipi_ts, 82)

seva <- tail(ipi_ts, n_total - 82)

cat("Estimation set:", length(sest), "observations\n")Estimation set: 82 observationscat("Evaluation set:", length(seva), "observations\n")Evaluation set: 49 observationsautoplot(decompose(sest)) +

labs(title = "Decomposition of IPI Manufacturing") +

theme_ts()

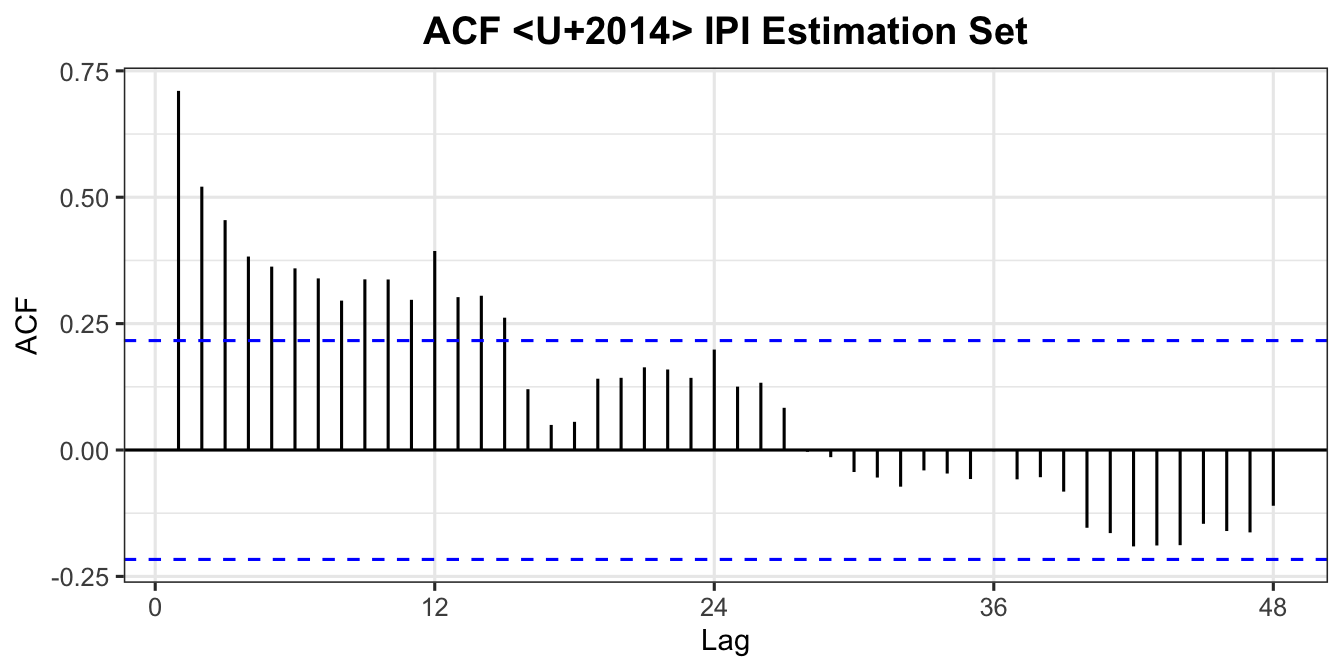

ggAcf(sest, lag.max = 48) +

labs(title = "ACF — IPI Estimation Set") +

theme_ts()

adf.test(sest)

Augmented Dickey-Fuller Test

data: sest

Dickey-Fuller = -3.9668, Lag order = 4, p-value = 0.0153

alternative hypothesis: stationaryEven if the ADF test indicates stationarity, the sinusoidal ACF pattern indicates a seasonal component — proceed with seasonal differencing.

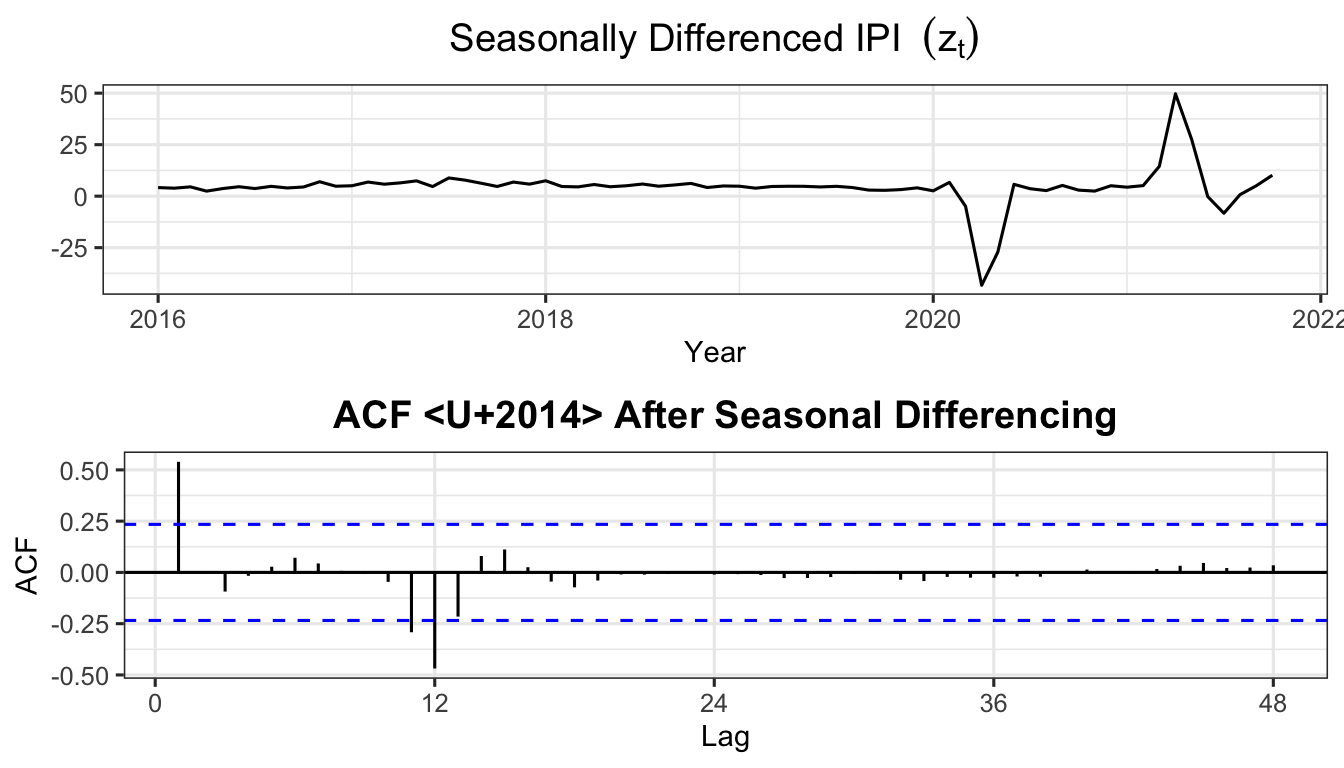

zt <- diff(sest, 12)

p_zt <- autoplot(zt) +

labs(title = expression("Seasonally Differenced IPI " ~ (z[t])),

x = "Year", y = "") +

theme_ts()

p_acfzt <- ggAcf(zt, lag.max = 48) +

labs(title = "ACF — After Seasonal Differencing") +

theme_ts()

grid.arrange(p_zt, p_acfzt, nrow = 2)

adf.test(zt)

Augmented Dickey-Fuller Test

data: zt

Dickey-Fuller = -3.0054, Lag order = 4, p-value = 0.1664

alternative hypothesis: stationaryIf the ADF test on \(z_t\) still fails to reject \(H_0\) (\(p > 0.05\)), apply a further first-order difference:

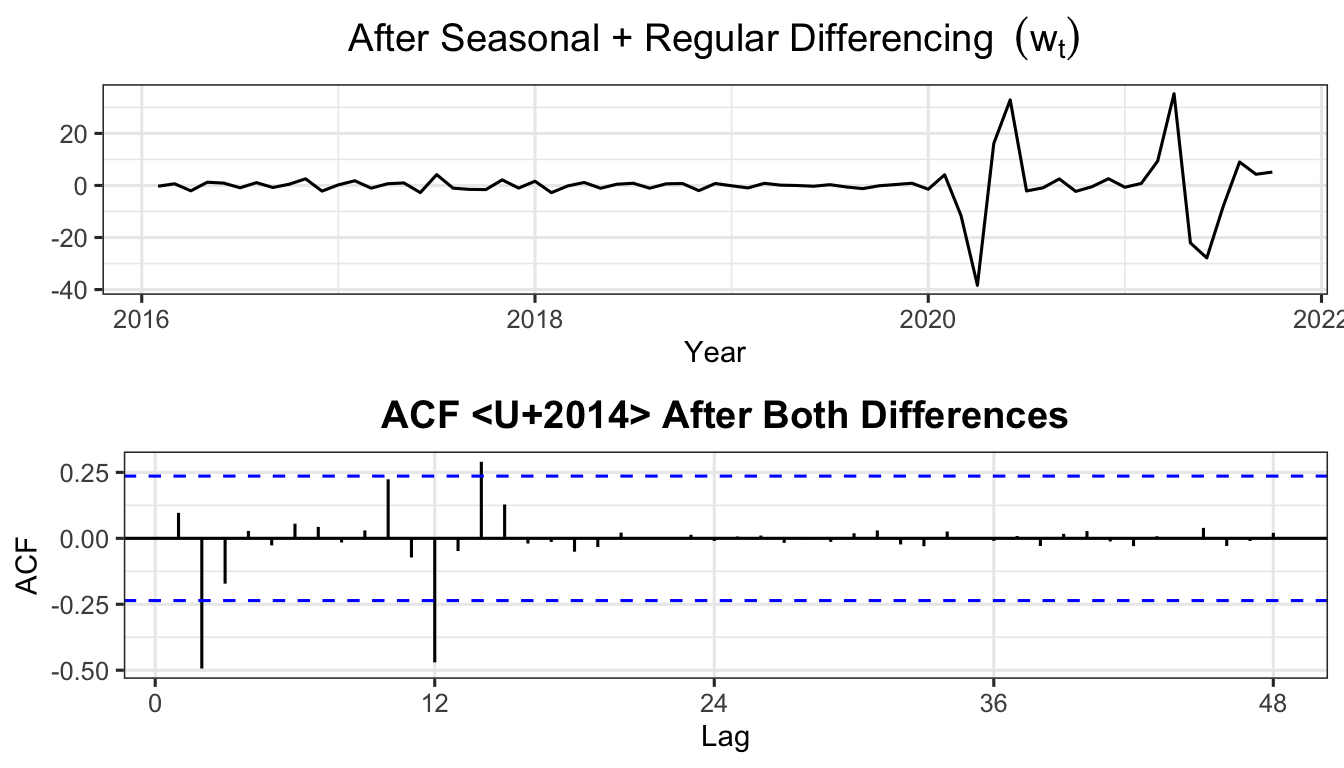

wt <- diff(zt, 1)

p_wt <- autoplot(wt) +

labs(title = expression("After Seasonal + Regular Differencing " ~ (w[t])),

x = "Year", y = "") +

theme_ts()

p_acfwt <- ggAcf(wt, lag.max = 48) +

labs(title = "ACF — After Both Differences") +

theme_ts()

grid.arrange(p_wt, p_acfwt, nrow = 2)

adf.test(wt)

Augmented Dickey-Fuller Test

data: wt

Dickey-Fuller = -5.9055, Lag order = 4, p-value = 0.01

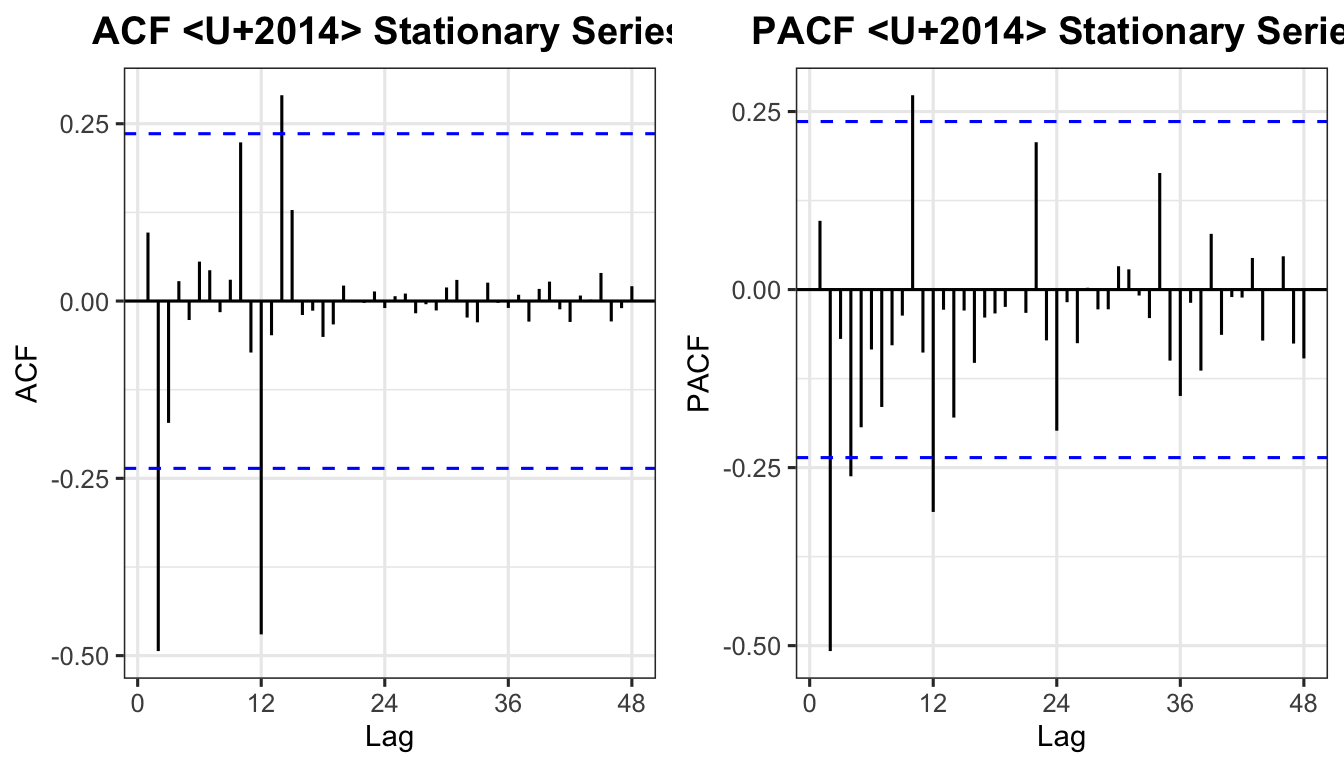

alternative hypothesis: stationaryp_acf_w <- ggAcf(wt, lag.max = 48) +

labs(title = "ACF — Stationary Series") + theme_ts()

p_pacf_w <- ggPacf(wt, lag.max = 48) +

labs(title = "PACF — Stationary Series") + theme_ts()

grid.arrange(p_acf_w, p_pacf_w, ncol = 2)

Reading the plots:

| Plot | Significant spike location | Interpretation |

|---|---|---|

| ACF | Lag 1 (non-seasonal) | MA(1) → \(q = 1\) |

| ACF | Lag 12 (seasonal) | SMA(1) → \(Q = 1\) |

| PACF | Lag 1 (non-seasonal) | AR(1) → \(p = 1\) |

| PACF | Lag 12 (seasonal) | SAR(1) → \(P = 1\) |

Suggested model: SARIMA\((1,1,1)(1,1,1)_{12}\)

Competing models: SARIMA\((2,1,2)(1,1,1)_{12}\) and SARIMA\((1,1,0)(1,1,1)_{12}\)

sest_tbl <- as_tsibble(sest)

seva_tbl <- as_tsibble(seva)

ipi_tbl <- as_tsibble(ipi_ts)

smodel1 <- sest_tbl |> model(ARIMA(value ~ pdq(1,1,1) + PDQ(1,1,1)))

smodel2 <- sest_tbl |> model(ARIMA(value ~ pdq(2,1,2) + PDQ(1,1,1)))

smodel3 <- sest_tbl |> model(ARIMA(value ~ pdq(1,1,0) + PDQ(1,1,1)))

report(smodel1)Series: value

Model: ARIMA(1,1,1)(1,1,1)[12]

Coefficients:

ar1 ma1 sar1 sma1

-0.3961 0.6660 -0.0953 -0.7322

s.e. 0.2099 0.1593 0.3314 0.4365

sigma^2 estimated as 44.88: log likelihood=-232.53

AIC=475.05 AICc=476.01 BIC=486.23Estimated equation for SARIMA\((1,1,1)(1,1,1)_{12}\):

\[ (1 - \hat\phi_1 B)(1 - B)(1 - \hat\Phi_1 B^{12})(1 - B^{12})\,y_t = (1 + \hat\theta_1 B)(1 + \hat\Theta_1 B^{12})\,\varepsilon_t \tag{30} \]

Exercise: Write the estimated equations for:

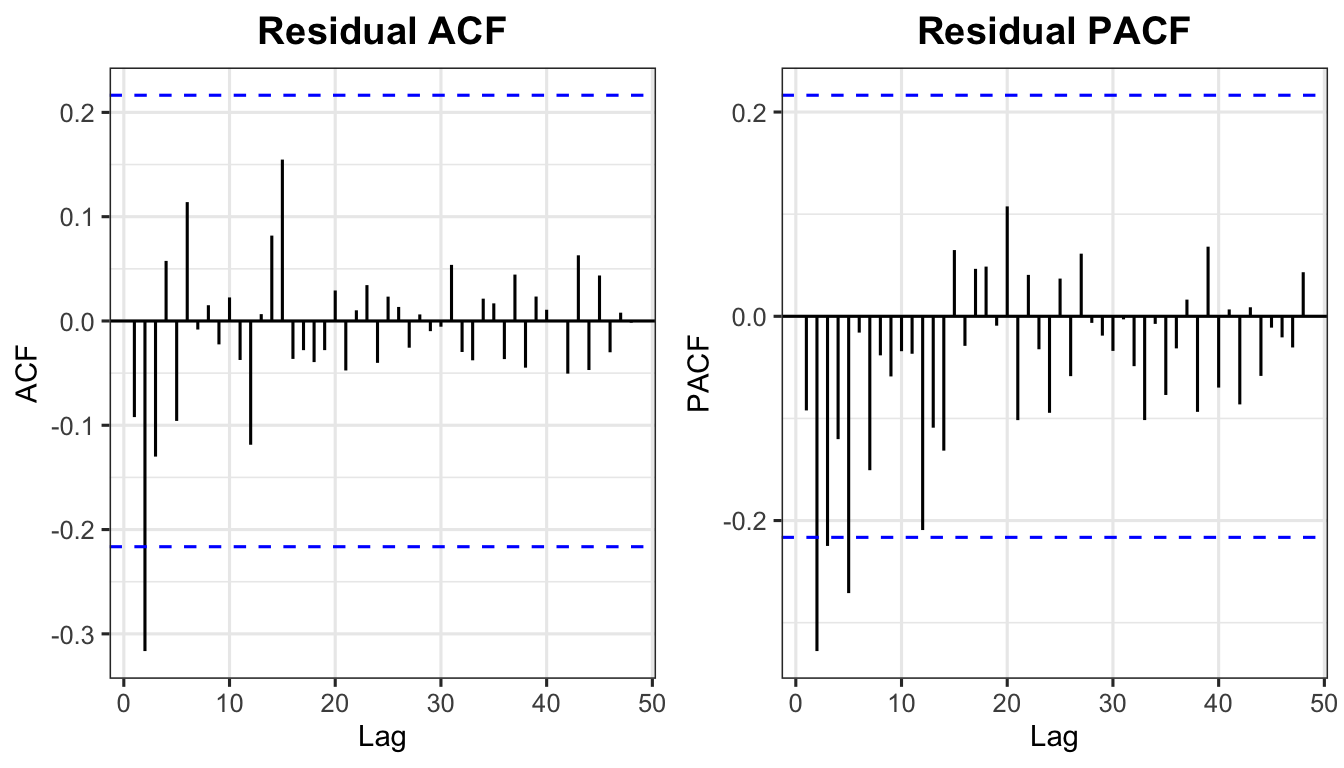

se1 <- residuals(smodel1)

p_ra <- ggAcf(se1$.resid, lag.max = 48) +

labs(title = "Residual ACF") + theme_ts()

p_rpa <- ggPacf(se1$.resid, lag.max = 48) +

labs(title = "Residual PACF") + theme_ts()

grid.arrange(p_ra, p_rpa, ncol = 2)

The Box-Pierce statistic:

\[ Q_{\text{calc}} = (T - d)\sum_{k=1}^{h} r_k^2 \tag{31} \]

The Ljung-Box statistic (preferred for small samples):

\[ Q^*_{\text{calc}} = T(T+2)\sum_{k=1}^{h}\frac{r_k^2}{T-k} \tag{32} \]

Both are approximately \(\chi^2\) distributed with \((h - p - q)\) degrees of freedom.

How many lags to use:

Box.test(se1$.resid, lag = 24, type = "Ljung-Box", fitdf = 4)

Box-Ljung test

data: se1$.resid

X-squared = 19.067, df = 20, p-value = 0.5174# Ljung-Box p-values for all three models

lb_results <- data.frame(

Model = c("SARIMA(1,1,1)(1,1,1)[12]",

"SARIMA(2,1,2)(1,1,1)[12]",

"SARIMA(1,1,0)(1,1,1)[12]"),

p_value = c(

Box.test(residuals(smodel1)$.resid, lag=24, type="Ljung-Box", fitdf=4)$p.value,

Box.test(residuals(smodel2)$.resid, lag=24, type="Ljung-Box", fitdf=6)$p.value,

Box.test(residuals(smodel3)$.resid, lag=24, type="Ljung-Box", fitdf=3)$p.value

)

)

lb_results$Decision <- ifelse(lb_results$p_value > 0.05,

"Fail to reject H0", "Reject H0")

lb_results$Conclusion <- ifelse(lb_results$p_value > 0.05,

"White noise", "Not white noise")

print(lb_results) Model p_value Decision Conclusion

1 SARIMA(1,1,1)(1,1,1)[12] 0.5174481 Fail to reject H0 White noise

2 SARIMA(2,1,2)(1,1,1)[12] 0.9650902 Fail to reject H0 White noise

3 SARIMA(1,1,0)(1,1,1)[12] 0.1480511 Fail to reject H0 White noiseAll models that pass the Ljung-Box test are candidate models. Select the best using AIC/BIC:

bind_rows(

glance(smodel1) |> mutate(Model = "SARIMA(1,1,1)(1,1,1)[12]"),

glance(smodel2) |> mutate(Model = "SARIMA(2,1,2)(1,1,1)[12]"),

glance(smodel3) |> mutate(Model = "SARIMA(1,1,0)(1,1,1)[12]")

) |>

select(Model, AIC, AICc, BIC) |>

arrange(AIC)# A tibble: 3 x 4

Model AIC AICc BIC

<chr> <dbl> <dbl> <dbl>

1 SARIMA(2,1,2)(1,1,1)[12] 457. 459. 473.

2 SARIMA(1,1,1)(1,1,1)[12] 475. 476. 486.

3 SARIMA(1,1,0)(1,1,1)[12] 478. 479. 487.The model with the lowest AIC, AICc, and BIC is selected as the best model.

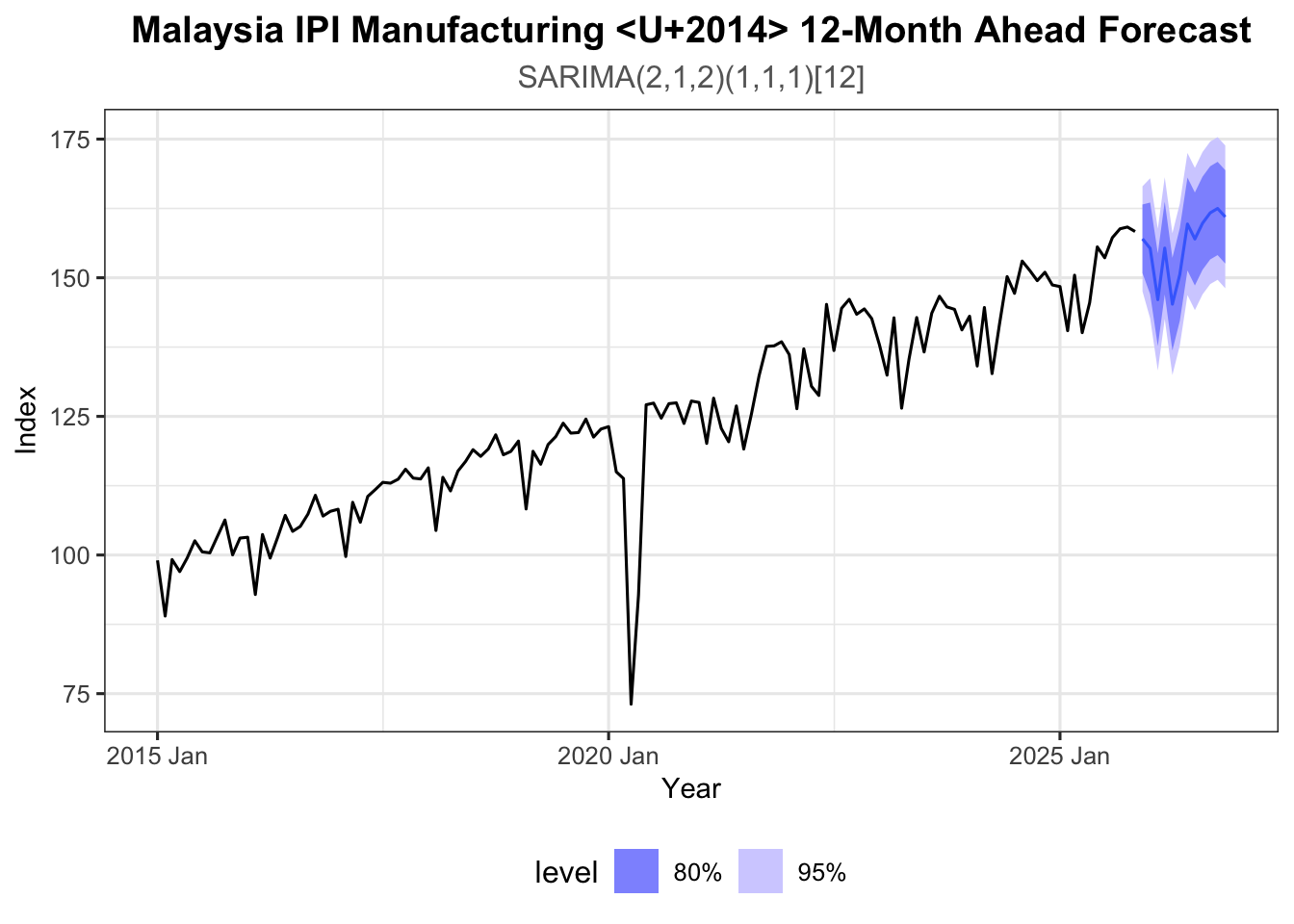

Use the best model (refitted to the full IPI series) to generate a 12-step-ahead forecast:

# Identify best model (lowest AIC among those with white noise residuals)

best_sarima <- sest_tbl |> model(ARIMA(value ~ pdq(2,1,2) + PDQ(1,1,1)))

best_sarima |>

refit(ipi_tbl) |>

forecast(h = 12) |>

autoplot(ipi_tbl, level = c(80, 95)) +

labs(title = "Malaysia IPI Manufacturing — 12-Month Ahead Forecast",

subtitle = "SARIMA(2,1,2)(1,1,1)[12]",

x = "Year", y = "Index") +

theme_ts()

| Stage | Task | Tools |

|---|---|---|

| 1 — Identification | Determine \(p\), \(d\), \(q\) (and \(P\), \(D\), \(Q\) for seasonal) | Time series plot, ACF, PACF, ADF test |

| 2 — Estimation | Estimate model parameters | OLS, Maximum Likelihood (R: ARIMA()) |

| 3 — Validation | Confirm residuals are white noise; select best model | Ljung-Box test, AIC, AICc, BIC |

| 4 — Application | Generate point forecasts and prediction intervals | forecast(), confidence bands |

| ACF | PACF | |

|---|---|---|

| AR(\(p\)) | Tails off | Cuts off after lag \(p\) |

| MA(\(q\)) | Cuts off after lag \(q\) | Tails off |

| ARMA(\(p\),\(q\)) | Tails off | Tails off |

| Non-stationary | Slow decay | Large at lag 1 |

| Seasonal | Peaks at seasonal lags (\(s\), \(2s\), …) | Peaks at seasonal lags |

| Criterion | Formula | Penalty |

|---|---|---|

| AIC | \(-2\log(L) + 2k\) | Moderate |

| AICc | \(\text{AIC} + \dfrac{2k(k+1)}{T-k-1}\) | Moderate (small sample correction) |

| BIC | \(-2\log(L) + k\log(T)\) | Stronger (grows with \(T\)) |

where $k = p + q + $ (1 if constant included, else 0).