By the end of this chapter, students should be able to:

Understand Time Series Fundamentals.

Identify Time Series Components.

Understand the Relationship Among Components.

Measure Forecast Performance.

Apply these concepts using R.

1.2 Definition

A time series is fundamentally defined as a time-oriented or chronological sequence of observations measured on a variable of interest. These observations are typically collected sequentially over time at fixed, equally spaced intervals, referred to as the sampling interval.

Depending on the context, time series data can take several forms:

Instantaneous measurements: A reading taken at a specific point in time, such as the viscosity of a chemical product at the moment it is measured.

Cumulative quantities: An accumulated total over the interval, such as the total product demand or sales during a month.

Summary statistics: A metric that reflects activity of the variable during the time period, such as the daily closing price of a stock.

1.2.1 Statistical and Mathematical Definition

A time series is modelled as a discrete-time stochastic process — a collection of random variables indexed according to the discrete time order in which they are obtained.

A time series of length \(n\) is represented as:

\[\{y_t : t = 1, 2, \ldots, n\}\]

where the subscript \(t\) denotes the discrete time period.

An important distinction:

Concept

Description

The Time Series Model

The theoretical sequence of underlying random variables — the ensemble of possibilities

The Realization

The actual historical sequence of data observed; a single realization of the stochastic process

A time series can be visualized via a time series plot.

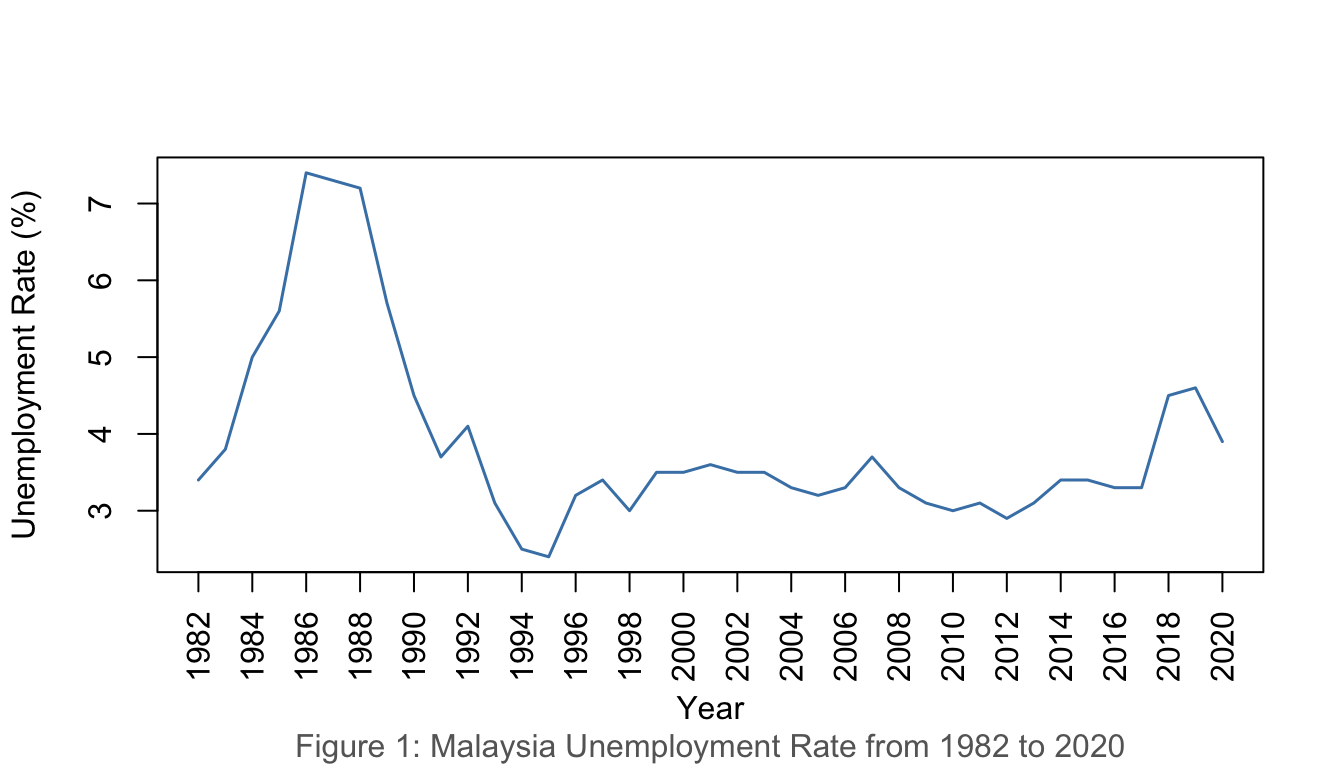

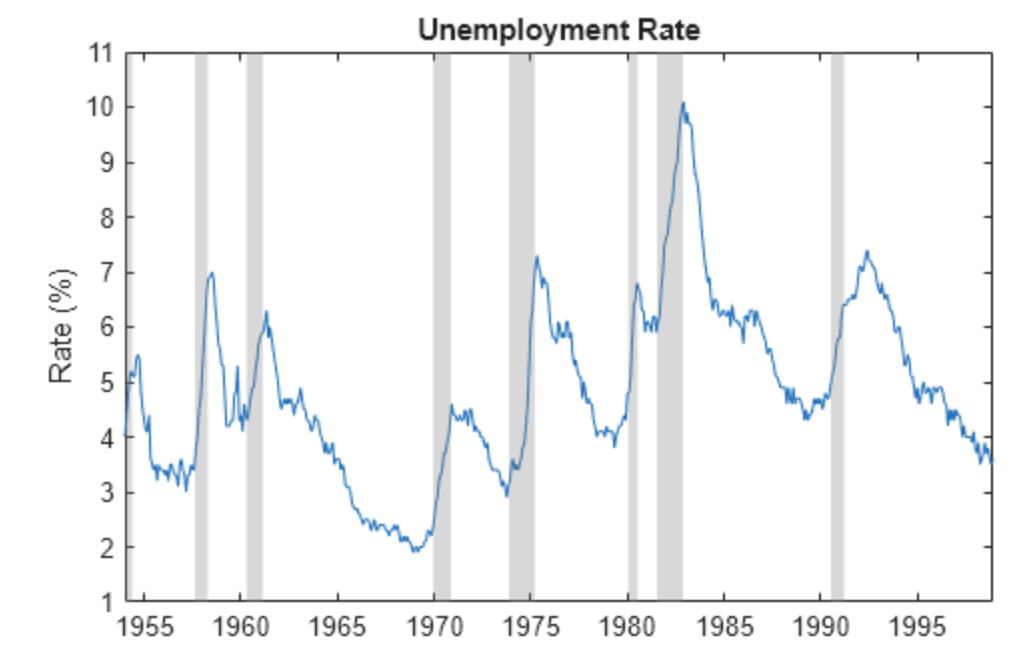

1.4.1 Example 1: Malaysia Unemployment Rate (1982–2020)

Show R Code

unrate <-read.csv("data/employment.csv")unratets <-ts(unrate$u_rate, start =1982)plot(unratets,ylab ="Unemployment Rate (%)", xlab ="Year", xaxt ="n",col ="steelblue", lwd =1.5)years <-seq(1982, 2020, by =2)axis(1, at = years, labels = years, las =2)title(sub ="Figure 1: Malaysia Unemployment Rate from 1982 to 2020",col.sub ="grey40")

Figure 1: Malaysia Unemployment Rate, 1982–2020

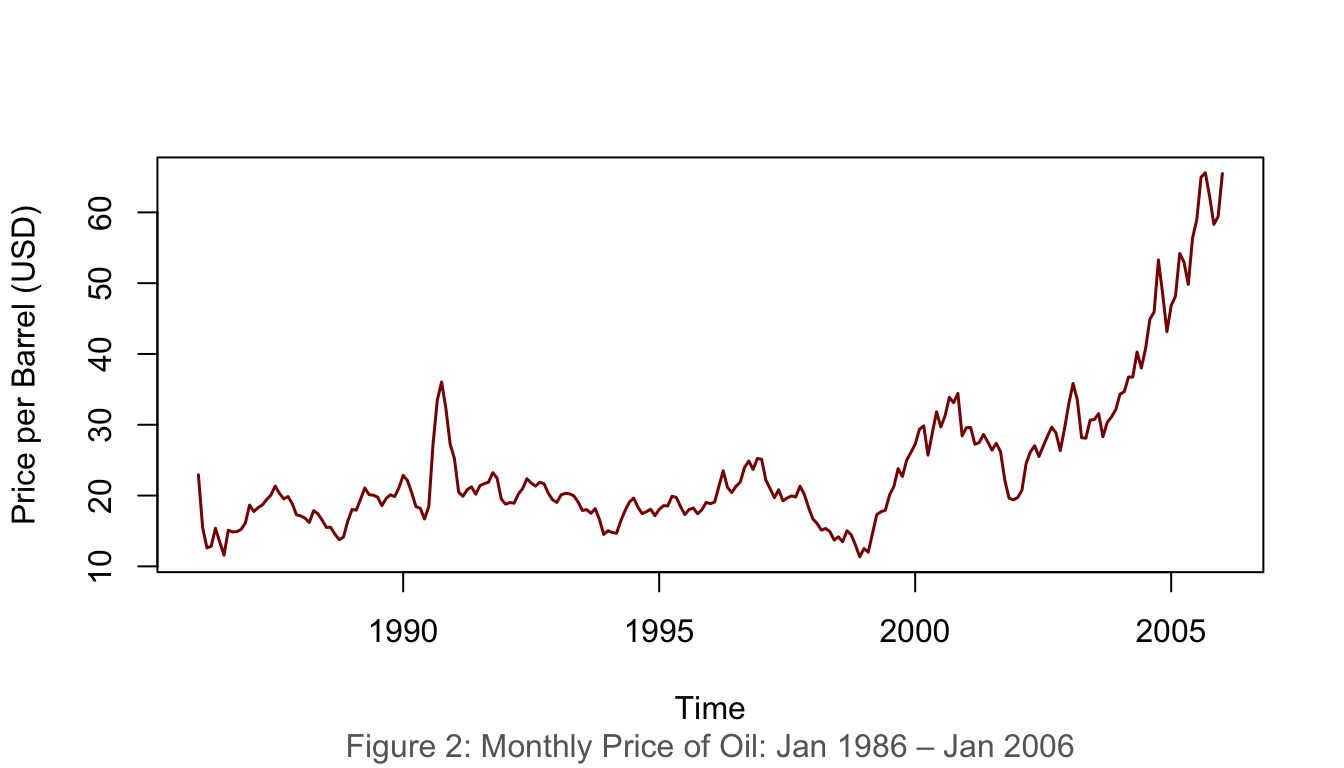

1.4.2 Example 2: Monthly Oil Price (Jan 1986 – Jan 2006)

Show R Code

data(oil.price)plot(oil.price, ylab ="Price per Barrel (USD)", type ="l",col ="darkred", lwd =1.5)title(sub ="Figure 2: Monthly Price of Oil: Jan 1986 – Jan 2006",col.sub ="grey40")

Figure 2: Monthly price of oil, January 1986 – January 2006

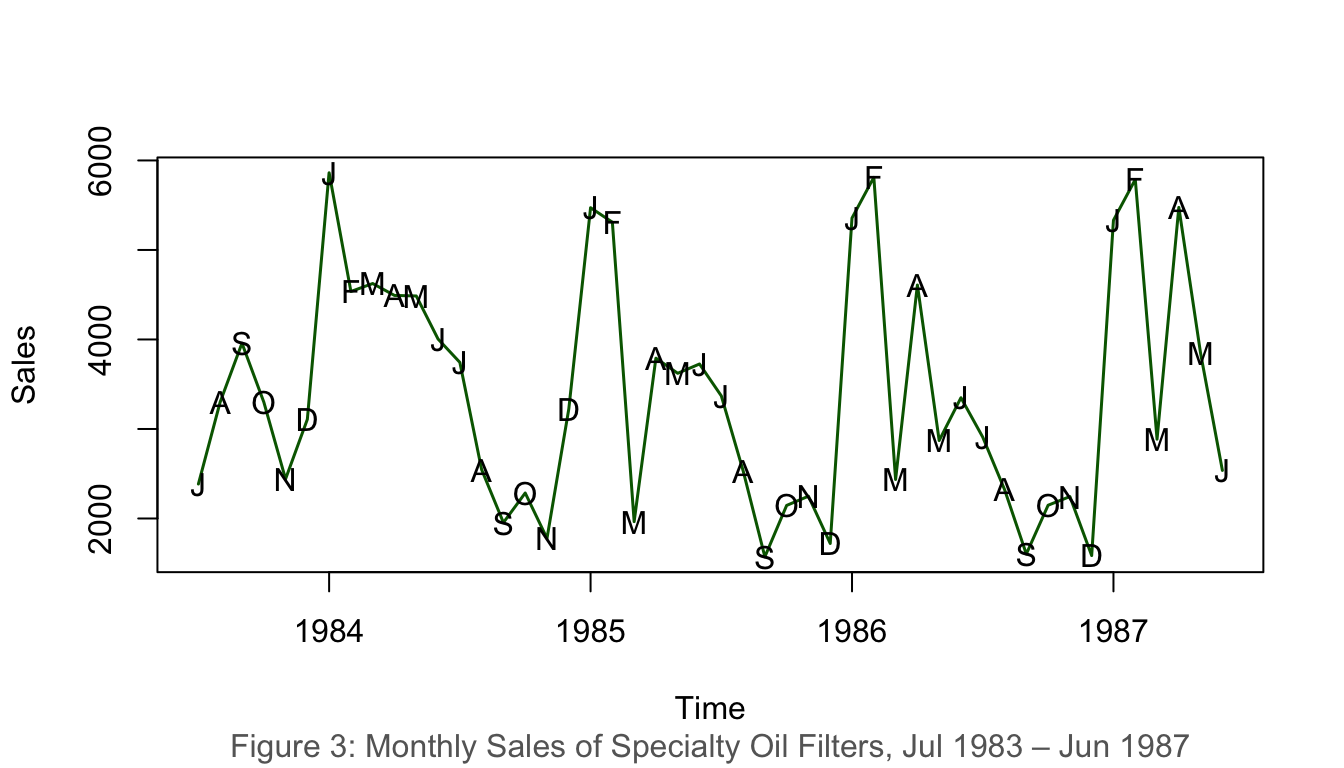

1.4.3 Example 3: Monthly Sales of Specialty Oil Filters (1983–1987)

Show R Code

data(oilfilters)plot(oilfilters, type ="l", ylab ="Sales", col ="darkgreen", lwd =1.5)points(y = oilfilters, x =time(oilfilters),pch =as.vector(season(oilfilters)))title(sub ="Figure 3: Monthly Sales of Specialty Oil Filters, Jul 1983 – Jun 1987",col.sub ="grey40")

Figure 3: Monthly sales of specialty oil filters, 1983–1987

1.5 Interpretation of Time Series Plot

When interpreting a time series plot, always include the following:

Element

Description

Minimum

The smallest value in the plot

Maximum

The largest value in the plot

Outliers

Values much further away from the rest of the data points

Trends

Patterns such as upward/downward movements or clusters

Example interpretation (Figure 1):Malaysia’s unemployment rate ranged from a minimum of 2.4% (1997) to a maximum of 7.4% (2020). The data shows a general downward trend from 1986 to 1997 and exhibits considerable fluctuation thereafter, with a sharp spike in 2020 likely attributed to the COVID-19 pandemic.

2 Components of Time Series

A time series is typically composed of four components:

Component

Notation

Description

Trend

\(T_t\)

Long-run direction of the series

Seasonal

\(S_t\)

Regular, repeating fluctuations within a fixed period

Cyclical

\(C_t\)

Long-wave rises and falls around the trend

Irregular/Random

\(I_t\)

Unpredictable, residual variation

2.1 Trend

The trend component describes the general upward or downward movements that characterise all economic and business activities.

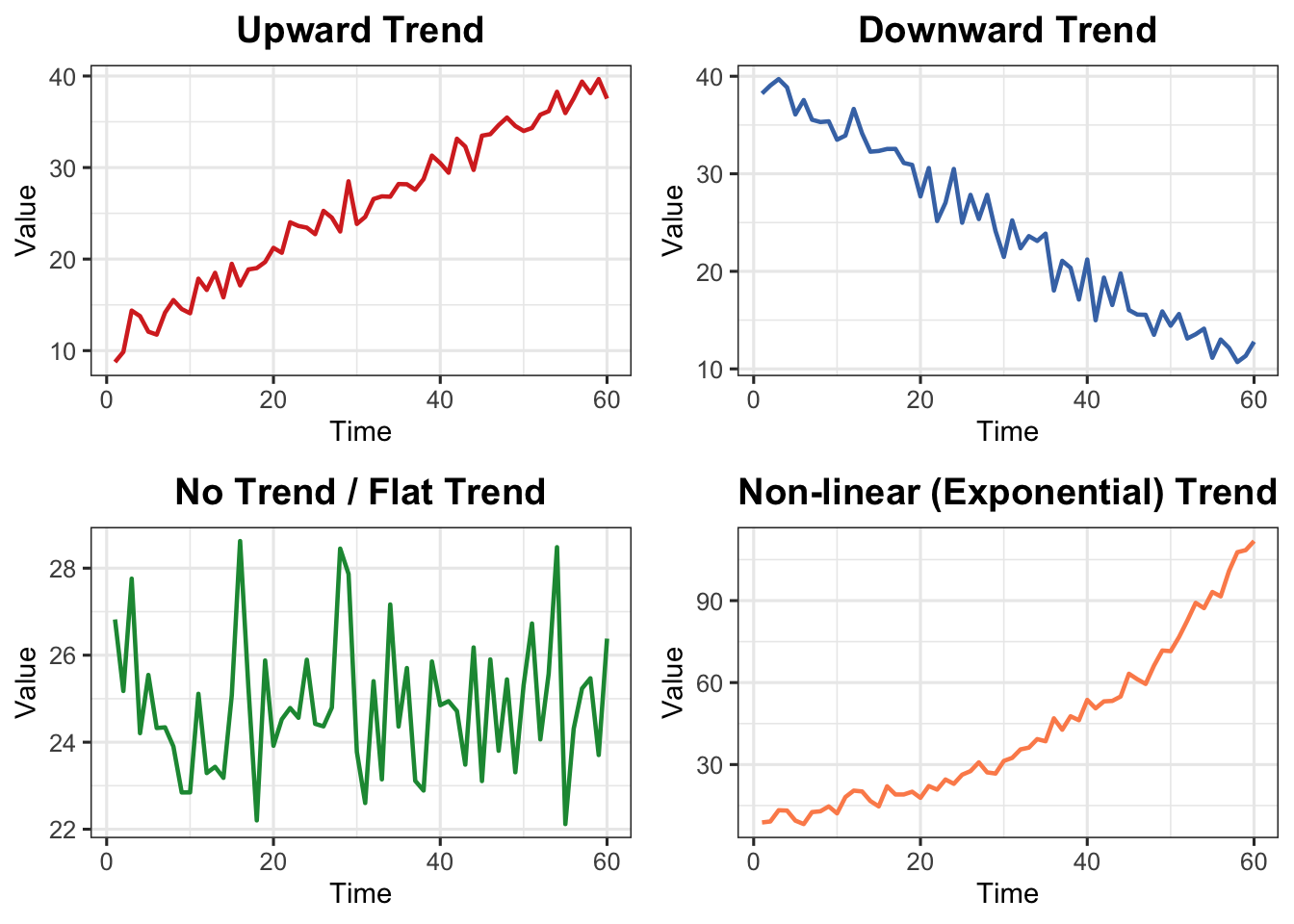

2.1.1 Types of Trends

Type

Description

Upward

Values increase over time

Downward

Values decrease over time

No Trend/Flat

Values remain relatively stable

Non-linear

Exhibits curvature — exponential growth, logarithmic decay, etc.

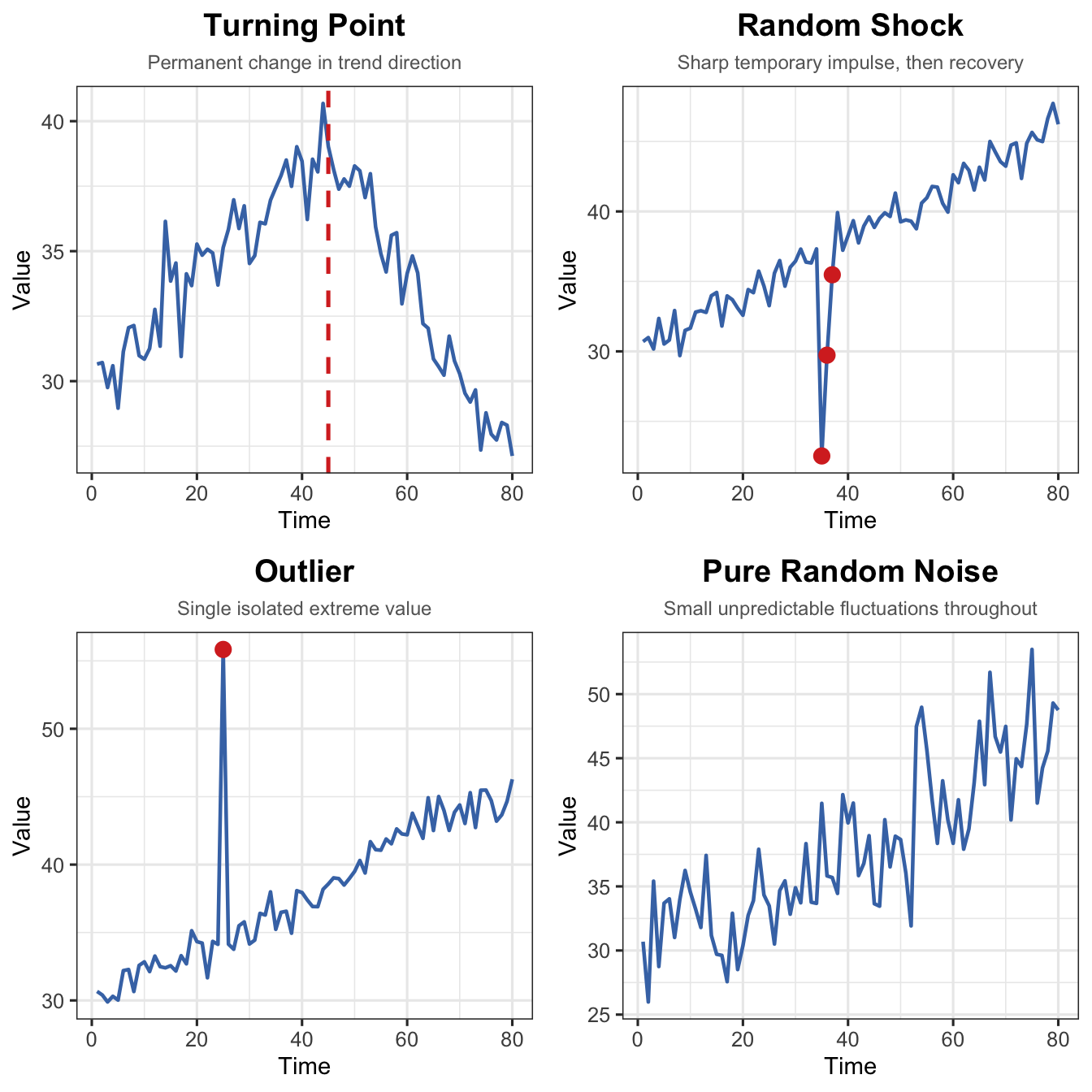

The irregular or random component is the portion that cannot be explained by trend, seasonal, or cyclical components. It has four distinct sub-types:

Sub-type

Key Characteristic

Visual Pattern

Turning Point

Trend permanently changes direction

Sustained shift in slope

Random Shock

Sudden, temporary spike or dip

Sharp impulse, then recovery

Outlier

One extreme isolated value

Single point far from neighbours

Pure Noise

Small unpredictable fluctuations

Irregular scatter around zero

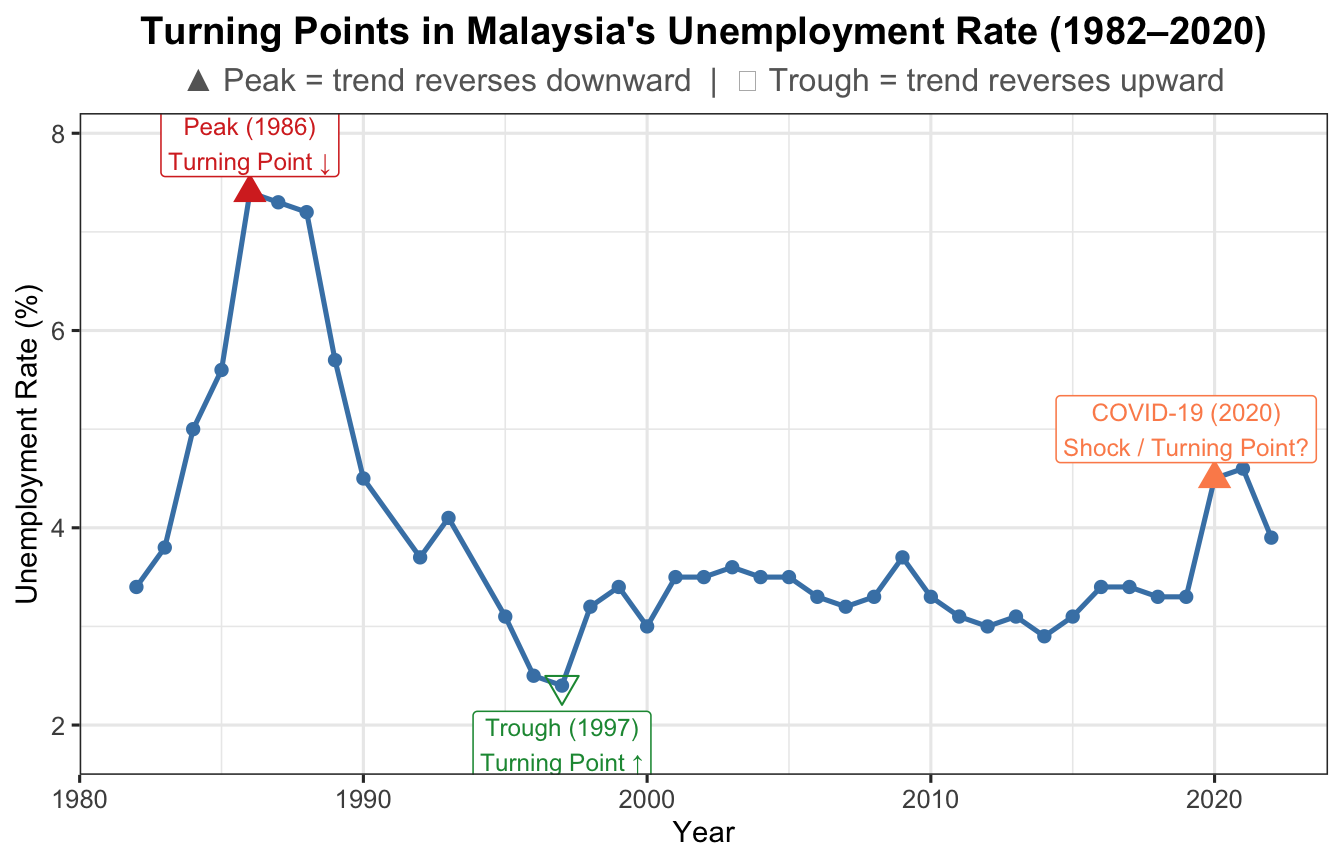

2.4.1 Turning Point

A turning point is where the long-run direction permanently reverses — from upward to downward or vice versa. Unlike a shock, the series does not recover to its prior direction.

Examples:

Introduction of robotic manufacturing permanently raises production.

Sudden change in consumer preference shifts demand to a new sustained level.

Policy change (e.g., new minimum wage legislation) permanently alters labour market dynamics.

Show R Code

unrate <-read.csv("data/employment.csv")df_u <-data.frame(Year =as.numeric(format(as.Date(unrate$date), "%Y")),u_rate = unrate$u_rate)ggplot(df_u, aes(x = Year, y = u_rate)) +geom_line(colour ="steelblue", linewidth =0.9) +geom_point(size =1.8, colour ="steelblue") +geom_point(data = df_u[df_u$Year ==1986, ],aes(x = Year, y = u_rate),colour ="#d73027", size =4, shape =17) +annotate("label", x =1986, y = df_u$u_rate[df_u$Year ==1986] +0.5,label ="Peak (1986)\nTurning Point ↓",colour ="#d73027", fill ="white", size =3.2, label.size =0.3) +geom_point(data = df_u[df_u$Year ==1997, ],aes(x = Year, y = u_rate),colour ="#1a9641", size =4, shape =25) +annotate("label", x =1997, y = df_u$u_rate[df_u$Year ==1997] -0.6,label ="Trough (1997)\nTurning Point ↑",colour ="#1a9641", fill ="white", size =3.2, label.size =0.3) +geom_point(data = df_u[df_u$Year ==2020, ],aes(x = Year, y = u_rate),colour ="#fc8d59", size =4, shape =17) +annotate("label", x =2019, y = df_u$u_rate[df_u$Year ==2020] +0.5,label ="COVID-19 (2020)\nShock / Turning Point?",colour ="#fc8d59", fill ="white", size =3.2, label.size =0.3) +labs(title ="Turning Points in Malaysia's Unemployment Rate (1982–2020)",subtitle ="▲ Peak = trend reverses downward | ▽ Trough = trend reverses upward",x ="Year", y ="Unemployment Rate (%)") +theme_ts()

Figure 9: Turning points in Malaysia’s unemployment rate (1982–2020)

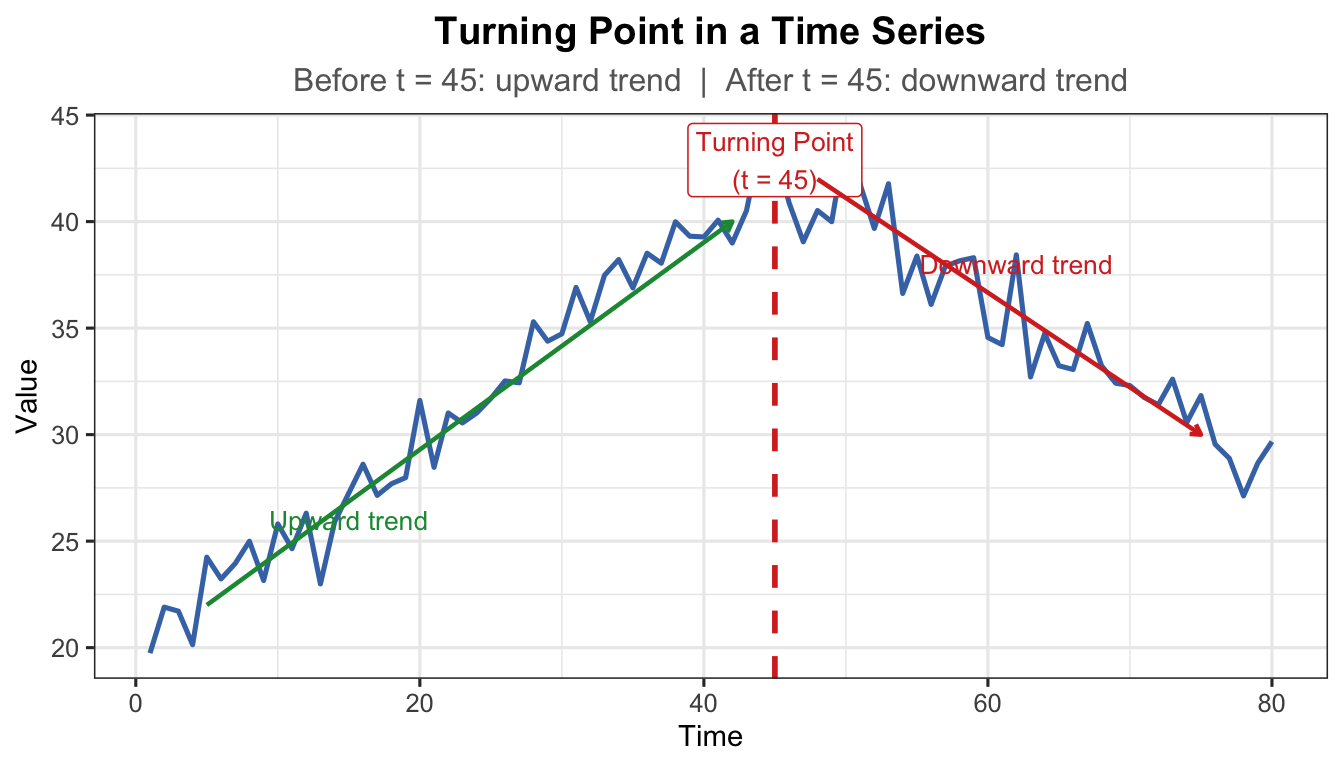

Show R Code

t_tp <-1:80# Before turning point: upward; after: downwardy_tp <-ifelse(t_tp <=45,20+0.5* t_tp,20+0.5*45-0.4* (t_tp -45)) +rnorm(80, 0, 1.2)df_tp <-data.frame(t = t_tp, y = y_tp)ggplot(df_tp, aes(x = t, y = y)) +geom_line(colour ="#4575b4", linewidth =0.9) +geom_vline(xintercept =45, linetype ="dashed", colour ="#d73027",linewidth =1) +annotate("label", x =45, y =max(y_tp) -1,label ="Turning Point\n(t = 45)", colour ="#d73027",fill ="white", size =3.5, label.size =0.3) +annotate("segment", x =5, xend =42, y =22, yend =40,arrow =arrow(length =unit(0.15, "cm")),colour ="#1a9641", linewidth =0.8) +annotate("text", x =15, y =26, label ="Upward trend",colour ="#1a9641", size =3.5) +annotate("segment", x =48, xend =75, y =42, yend =30,arrow =arrow(length =unit(0.15, "cm")),colour ="#d73027", linewidth =0.8) +annotate("text", x =62, y =38, label ="Downward trend",colour ="#d73027", size =3.5) +labs(title ="Turning Point in a Time Series",subtitle ="Before t = 45: upward trend | After t = 45: downward trend",x ="Time", y ="Value") +theme_ts()

Figure 10: Turning point — the trend permanently reverses direction at the marked point

Note

Turning point vs. Random Shock: A turning point results in a permanent direction change. After a random shock, the series recovers toward its previous level.

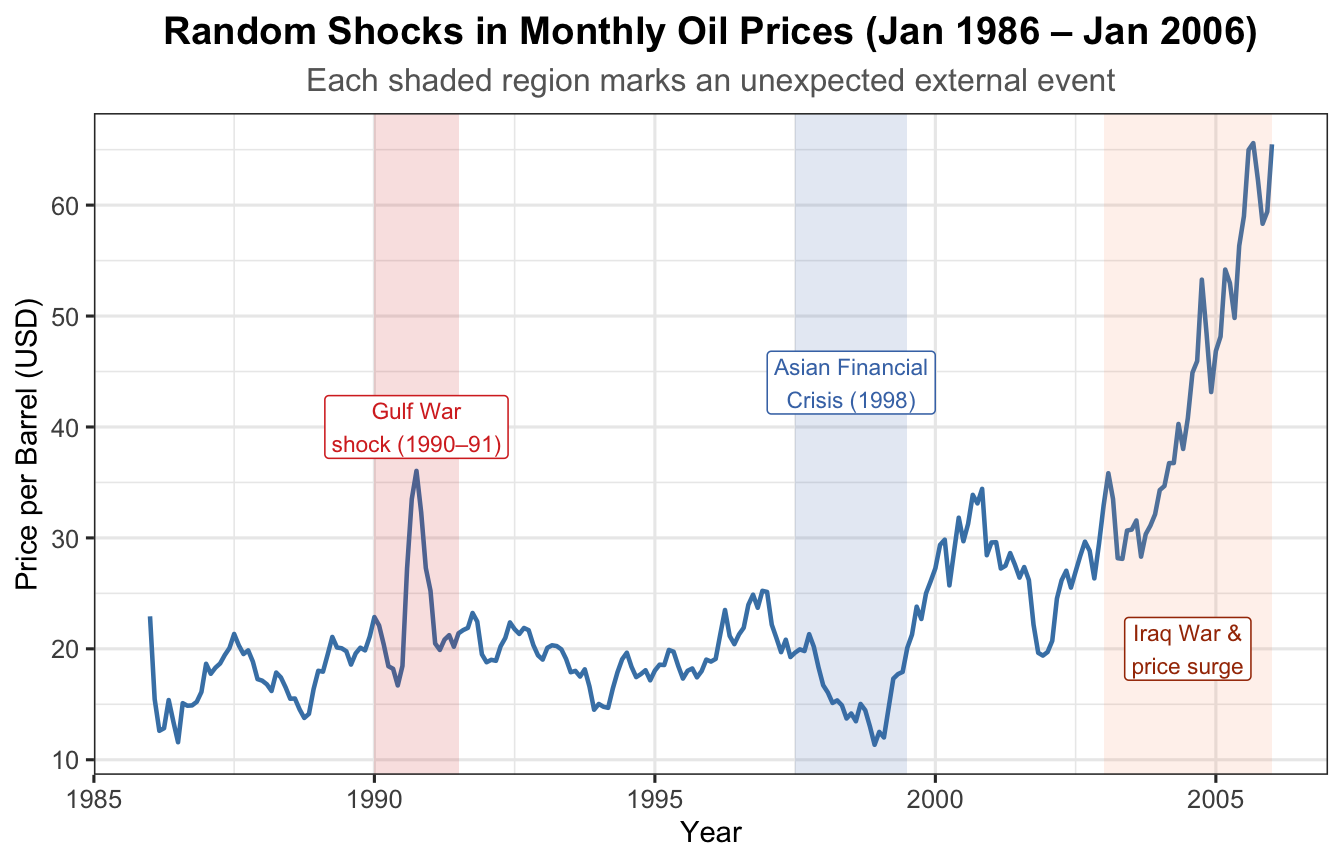

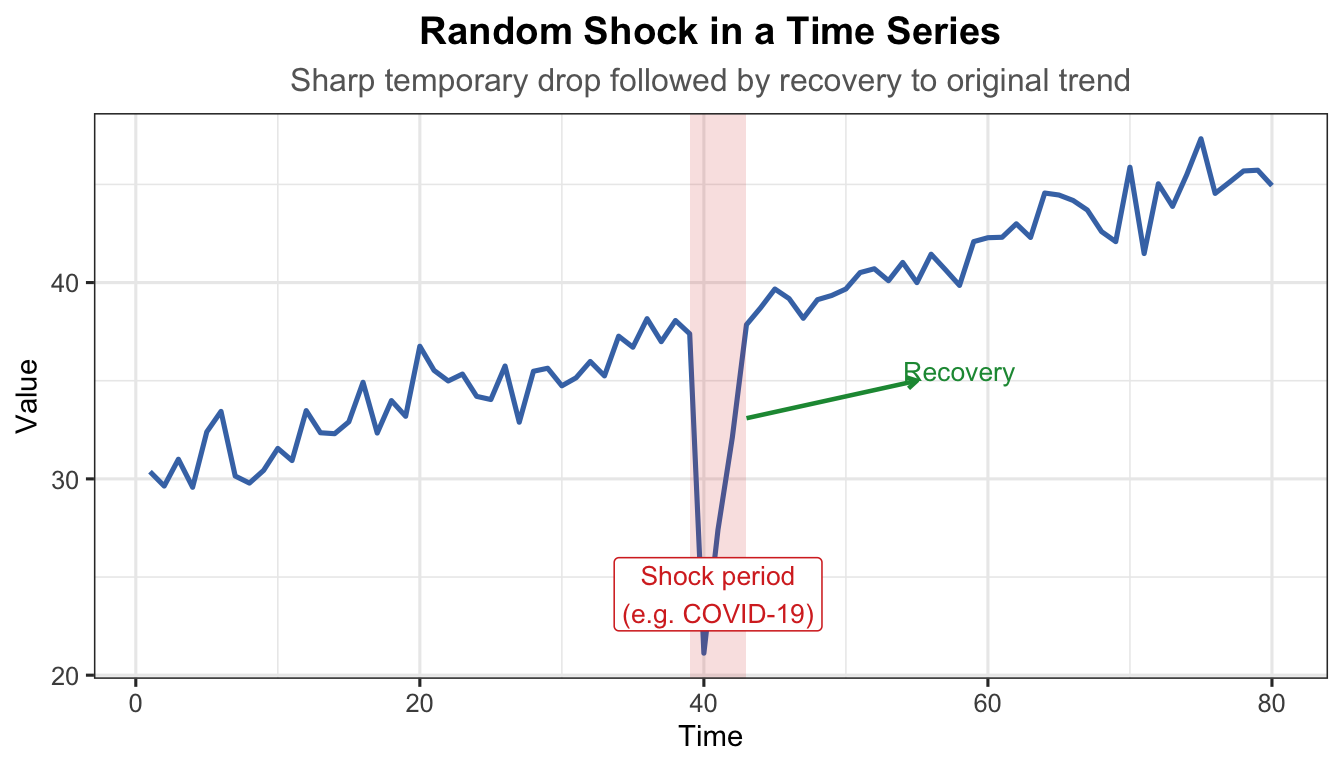

2.4.2 Random Shock

A random shock is an abrupt, temporary spike or drop caused by an unexpected external event. The series typically recovers toward its prior level once the event passes.

Examples:

Crude oil price sudden drop due to COVID-19.

Production of masks increasing tremendously during the pandemic.

Stock market crash following a geopolitical crisis or natural disaster.

Show R Code

data(oil.price)oil_df <-data.frame(Date =as.numeric(time(oil.price)),Price =as.numeric(oil.price))ggplot(oil_df, aes(x = Date, y = Price)) +geom_line(colour ="steelblue", linewidth =0.8) +annotate("rect", xmin =1990, xmax =1991.5,ymin =-Inf, ymax =Inf, alpha =0.15, fill ="#d73027") +annotate("label", x =1990.75, y =40,label ="Gulf War\nshock (1990–91)",colour ="#d73027", fill ="white", size =3, label.size =0.3) +annotate("rect", xmin =1997.5, xmax =1999.5,ymin =-Inf, ymax =Inf, alpha =0.15, fill ="#4575b4") +annotate("label", x =1998.5, y =44,label ="Asian Financial\nCrisis (1998)",colour ="#4575b4", fill ="white", size =3, label.size =0.3) +annotate("rect", xmin =2003, xmax =2006,ymin =-Inf, ymax =Inf, alpha =0.12, fill ="#fc8d59") +annotate("label", x =2004.5, y =20,label ="Iraq War &\nprice surge",colour ="#a63603", fill ="white", size =3, label.size =0.3) +labs(title ="Random Shocks in Monthly Oil Prices (Jan 1986 – Jan 2006)",subtitle ="Each shaded region marks an unexpected external event",x ="Year", y ="Price per Barrel (USD)") +theme_ts()

Figure 11: Random shocks in monthly oil prices (Jan 1986 – Jan 2006)

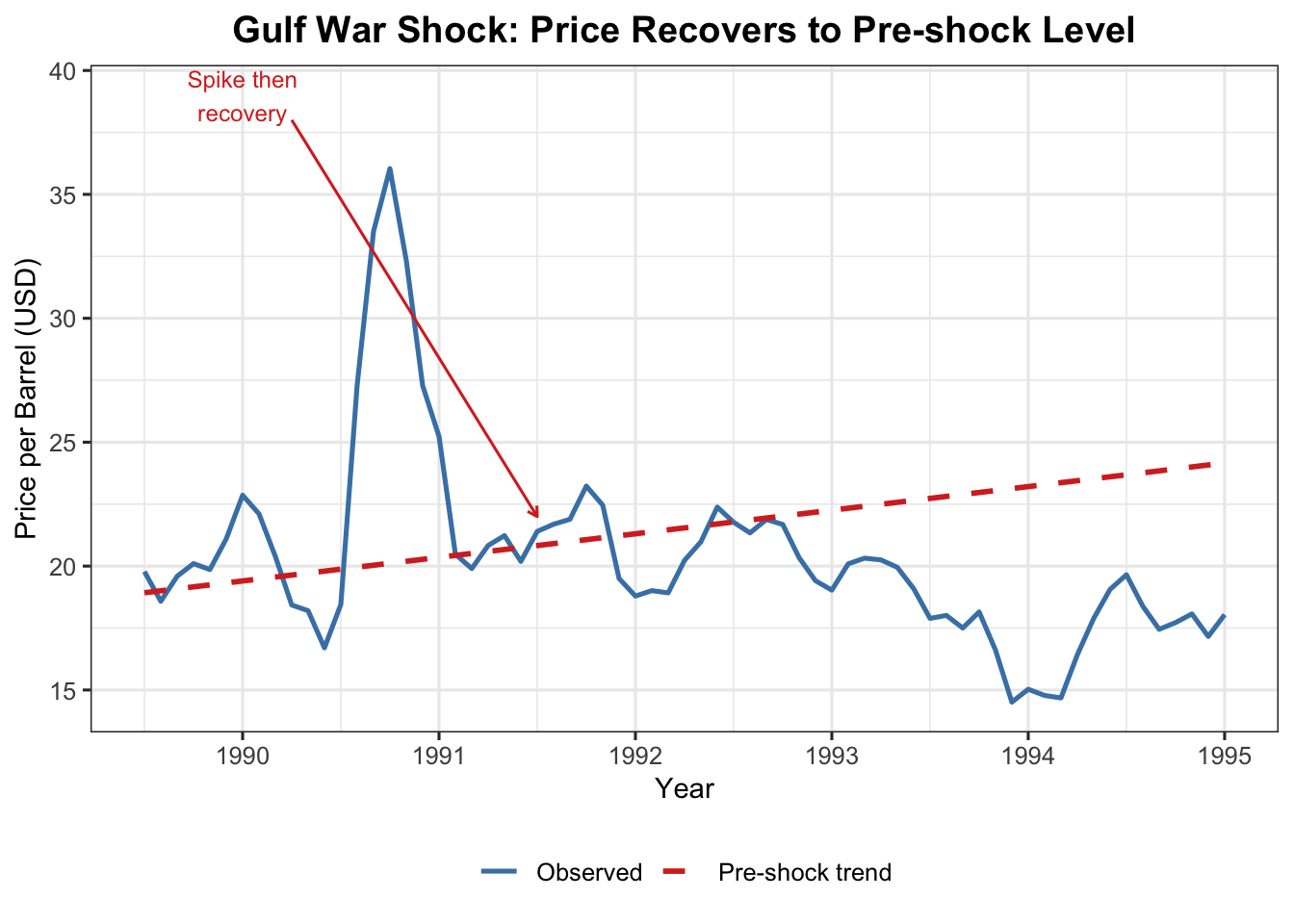

Show R Code

oil_sub <- oil_df[oil_df$Date >=1989.5& oil_df$Date <=1995, ]lm_pre <-lm(Price ~ Date, data = oil_df[oil_df$Date <1990, ])oil_sub$trend <-predict(lm_pre, newdata =data.frame(Date = oil_sub$Date))ggplot(oil_sub, aes(x = Date)) +geom_line(aes(y = Price, colour ="Observed"), linewidth =0.9) +geom_line(aes(y = trend, colour ="Pre-shock trend"),linetype ="dashed", linewidth =1) +annotate("segment", x =1990.25, xend =1991.5, y =38, yend =22,arrow =arrow(length =unit(0.15, "cm")), colour ="#d73027") +annotate("text", x =1990, y =39, label ="Spike then\nrecovery",colour ="#d73027", size =3.2) +scale_colour_manual(values =c("Observed"="steelblue","Pre-shock trend"="#d73027")) +labs(title ="Gulf War Shock: Price Recovers to Pre-shock Level",x ="Year", y ="Price per Barrel (USD)", colour =NULL) +theme_ts()

Figure 12: Gulf War shock (1990–91): price spikes then recovers to prior trend

Show R Code

t_sh <-1:80trend_sh <-30+0.2* t_shnoise_sh <-rnorm(80, 0, 1.2)shock <-rep(0, 80)shock[40] <--18# sudden sharp downward shockshock[41] <--10shock[42] <--4# gradual recoveryy_sh <- trend_sh + shock + noise_shdf_sh <-data.frame(t = t_sh, y = y_sh)ggplot(df_sh, aes(x = t, y = y)) +geom_line(colour ="#4575b4", linewidth =0.9) +annotate("rect", xmin =39, xmax =43, ymin =-Inf, ymax =Inf,alpha =0.15, fill ="#d73027") +annotate("label", x =41, y =min(y_sh) +3,label ="Shock period\n(e.g. COVID-19)", colour ="#d73027",fill ="white", size =3.5, label.size =0.3) +annotate("segment", x =43, xend =55, y = y_sh[42] +1, yend =35,arrow =arrow(length =unit(0.15, "cm")), colour ="#1a9641",linewidth =0.8) +annotate("text", x =58, y =35.5, label ="Recovery",colour ="#1a9641", size =3.5) +labs(title ="Random Shock in a Time Series",subtitle ="Sharp temporary drop followed by recovery to original trend",x ="Time", y ="Value") +theme_ts()

Figure 13: Random shock — a sudden spike followed by recovery to the previous level

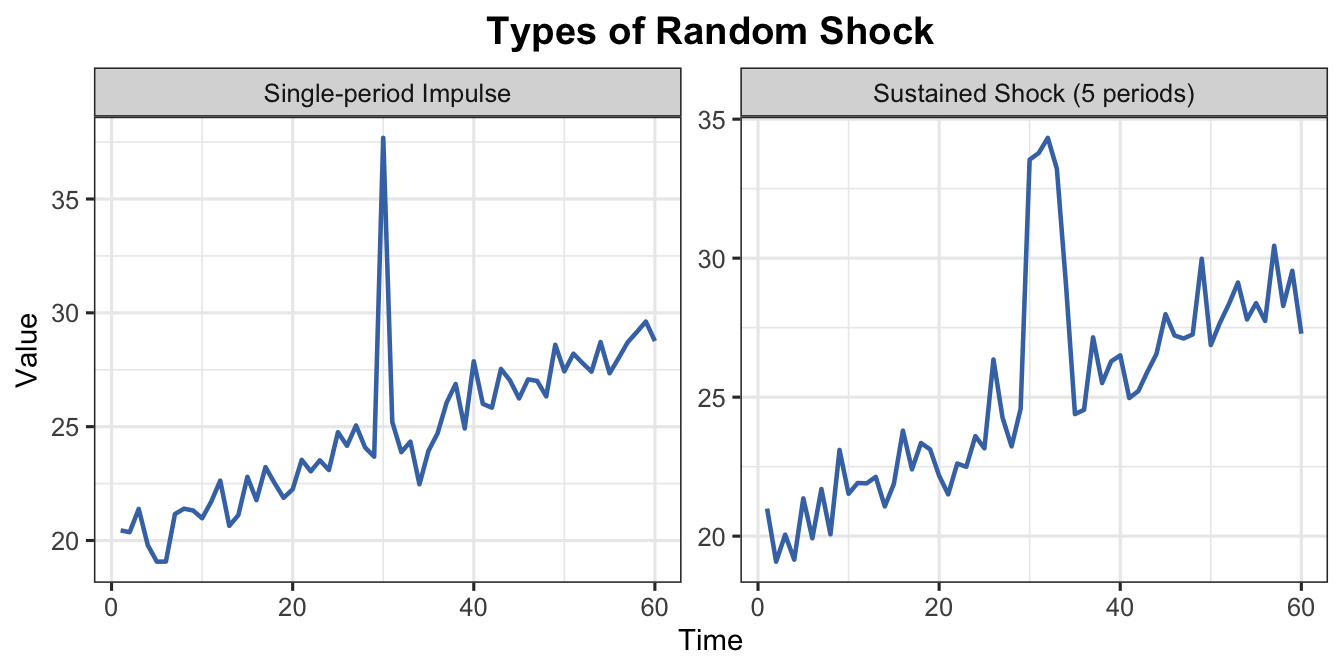

Show R Code

t2 <-1:60base <-20+0.15* t2# Single-period impulsey_imp <- base +rnorm(60, 0, 0.8)y_imp[30] <- y_imp[30] +12# Multi-period sustained shock (e.g. supply chain disruption for 5 months)shock_sus <-rep(0, 60)shock_sus[30:34] <-c(8, 10, 9, 7, 4)y_sus <- base + shock_sus +rnorm(60, 0, 0.8)df_imp <-data.frame(t = t2, y = y_imp, type ="Single-period Impulse")df_sus <-data.frame(t = t2, y = y_sus, type ="Sustained Shock (5 periods)")df_cmp <-rbind(df_imp, df_sus)ggplot(df_cmp, aes(x = t, y = y)) +geom_line(colour ="#4575b4", linewidth =0.8) +facet_wrap(~type, scales ="free_y") +labs(title ="Types of Random Shock",x ="Time", y ="Value") +theme_ts()

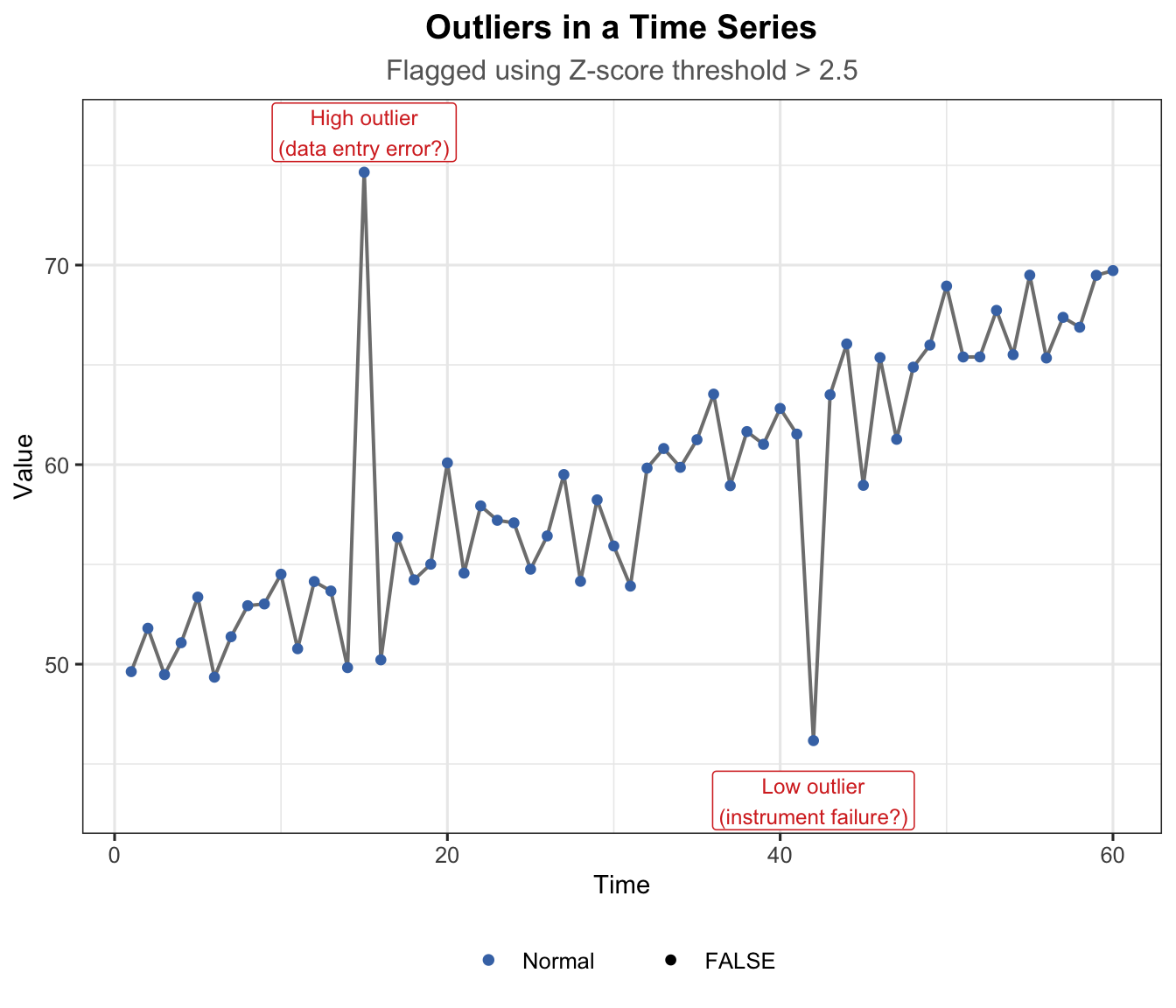

An outlier is an isolated data point that significantly deviates from the overall pattern. Unlike a random shock (which spans several periods), an outlier is typically a single observation.

Outliers arise from: errors in data collection, measurement instrument failure, or genuinely unusual one-off events.

Show R Code

t_out <-1:60y_out <-50+0.3* t_out +rnorm(60, 0, 2)# Inject outliersy_out[15] <- y_out[15] +20# high outliery_out[42] <- y_out[42] -18# low outlier# Z-score to flag outliersz_scores <-abs(scale(y_out))is_outlier <- z_scores >2.5df_out <-data.frame(t = t_out, y = y_out, outlier =as.vector(is_outlier))ggplot(df_out, aes(x = t, y = y)) +geom_line(colour ="grey50", linewidth =0.7) +geom_point(aes(colour = outlier, size = outlier)) +scale_colour_manual(values =c("FALSE"="#4575b4", "TRUE"="#d73027"),labels =c("FALSE"="Normal", "TRUE"="Outlier")) +scale_size_manual(values =c("FALSE"=1.5, "TRUE"=3.5)) +annotate("label", x =15, y = y_out[15] +2,label ="High outlier\n(data entry error?)",colour ="#d73027", fill ="white", size =3.2, label.size =0.3) +annotate("label", x =42, y = y_out[42] -3,label ="Low outlier\n(instrument failure?)",colour ="#d73027", fill ="white", size =3.2, label.size =0.3) +labs(title ="Outliers in a Time Series",subtitle ="Flagged using Z-score threshold > 2.5",x ="Time", y ="Value", colour =NULL, size =NULL) +theme_ts()

Figure 15: Outliers in a time series — isolated extreme data points

How to detect outliers:

Visual inspection of the time series plot.

Z-score method — flag where \(|z_t| = |\frac{y_t - \bar{y}}{s}| > 2.5\).

Decomposition residuals — inspect the irregular component after removing trend and seasonal effects.

How to deal with outliers:

Strategy

When to Use

Remove

Confirmed data entry errors or instrument failures

Winsorize

Replace with boundary value (5th/95th percentile)

Impute

Replace with average of neighbours

Robust models

Use outlier-resistant forecasting techniques

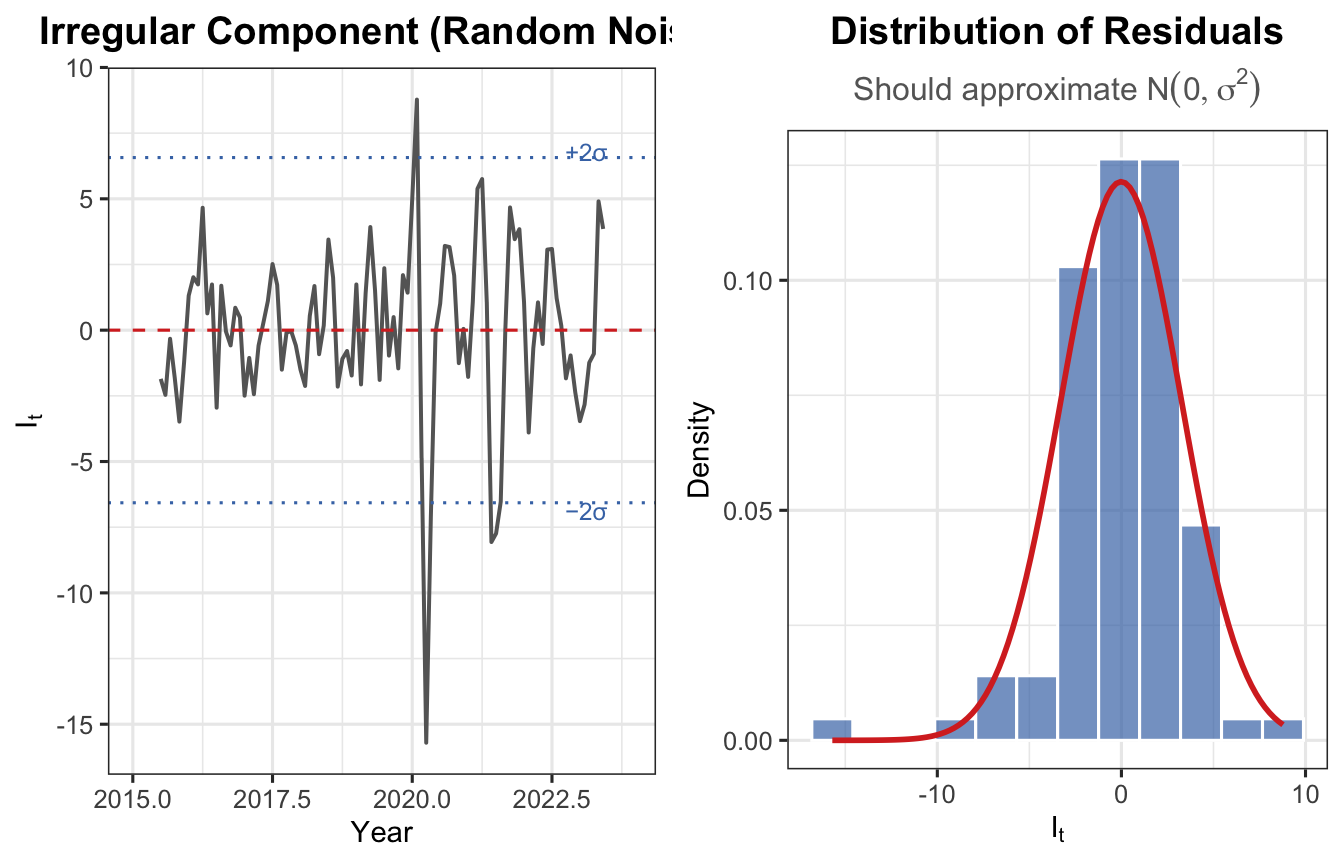

2.4.4 Random (Pure Noise)

The random sub-component refers to small, unpredictable fluctuations that remain after all systematic effects are removed. Also called the residual or error term.

Random errors are expected to be \(I_t \sim N(0, \sigma^2)\) and uncorrelated across time.

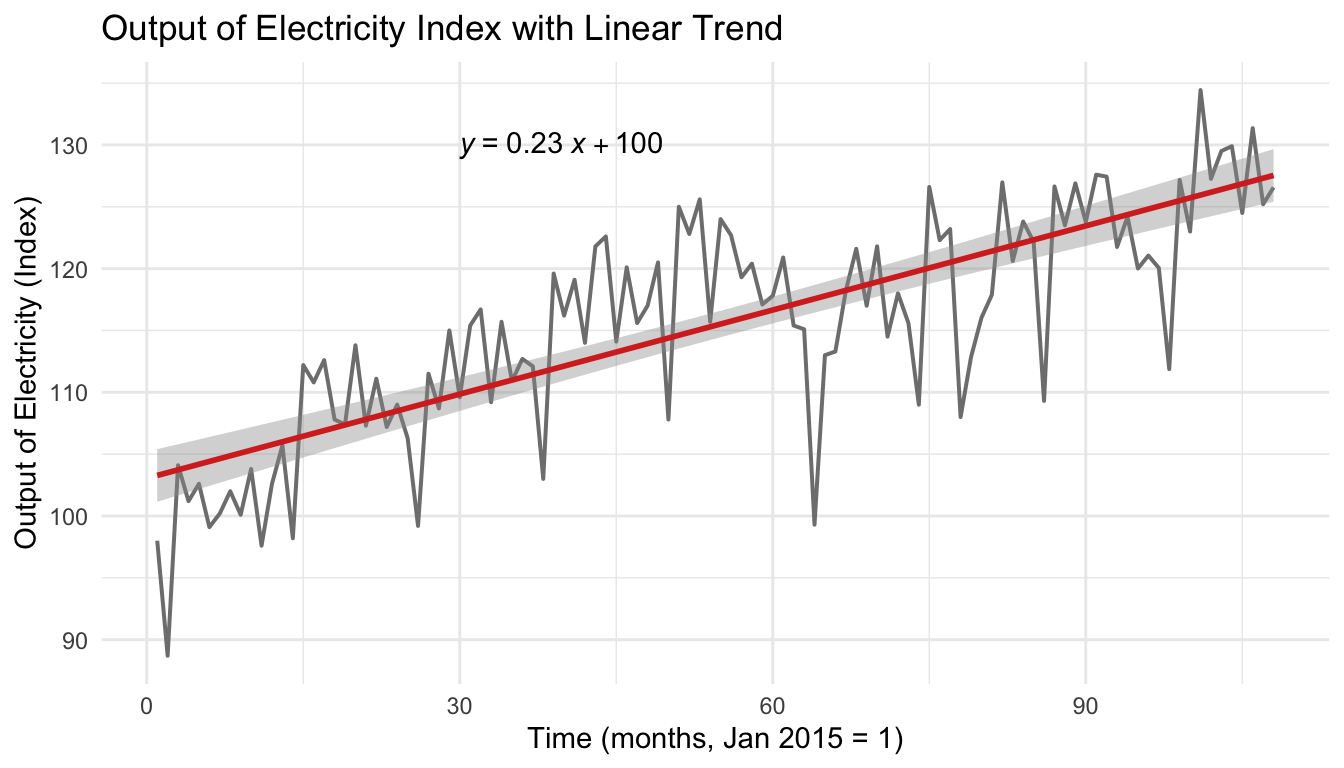

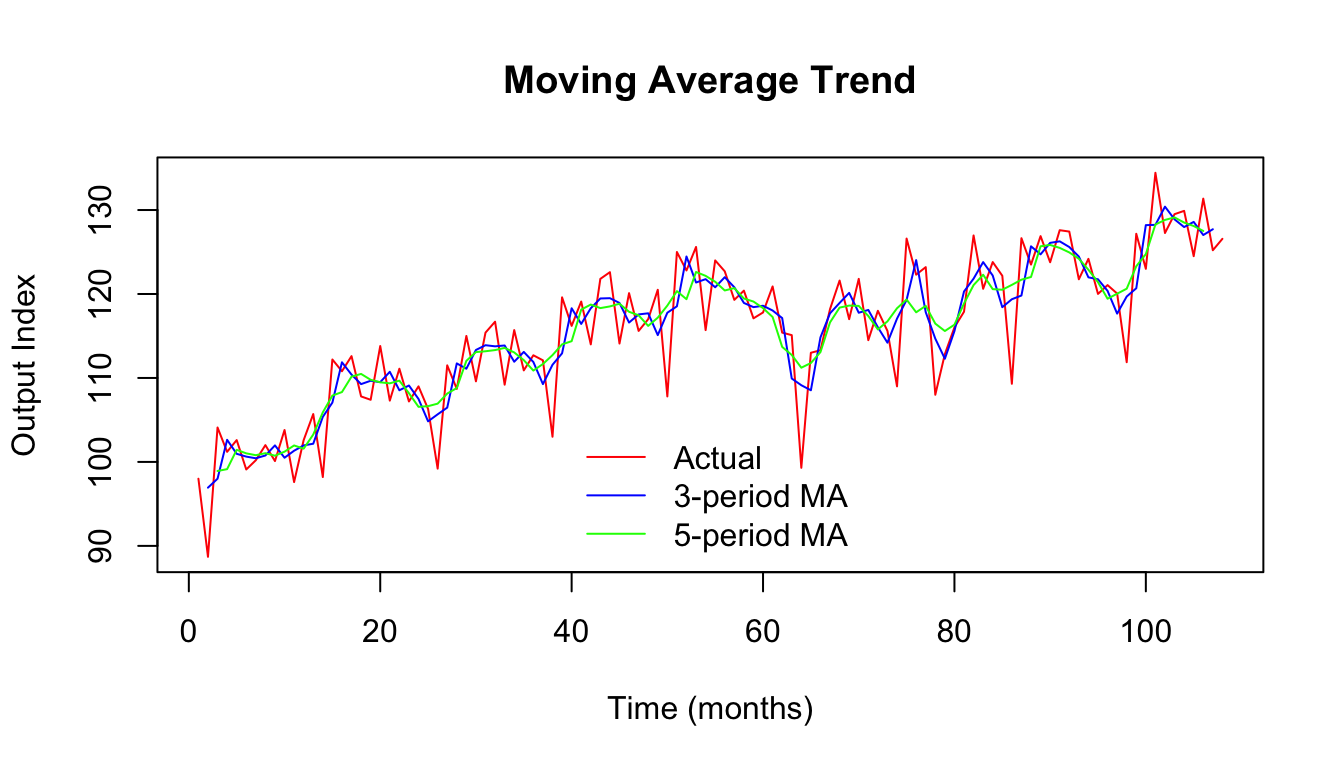

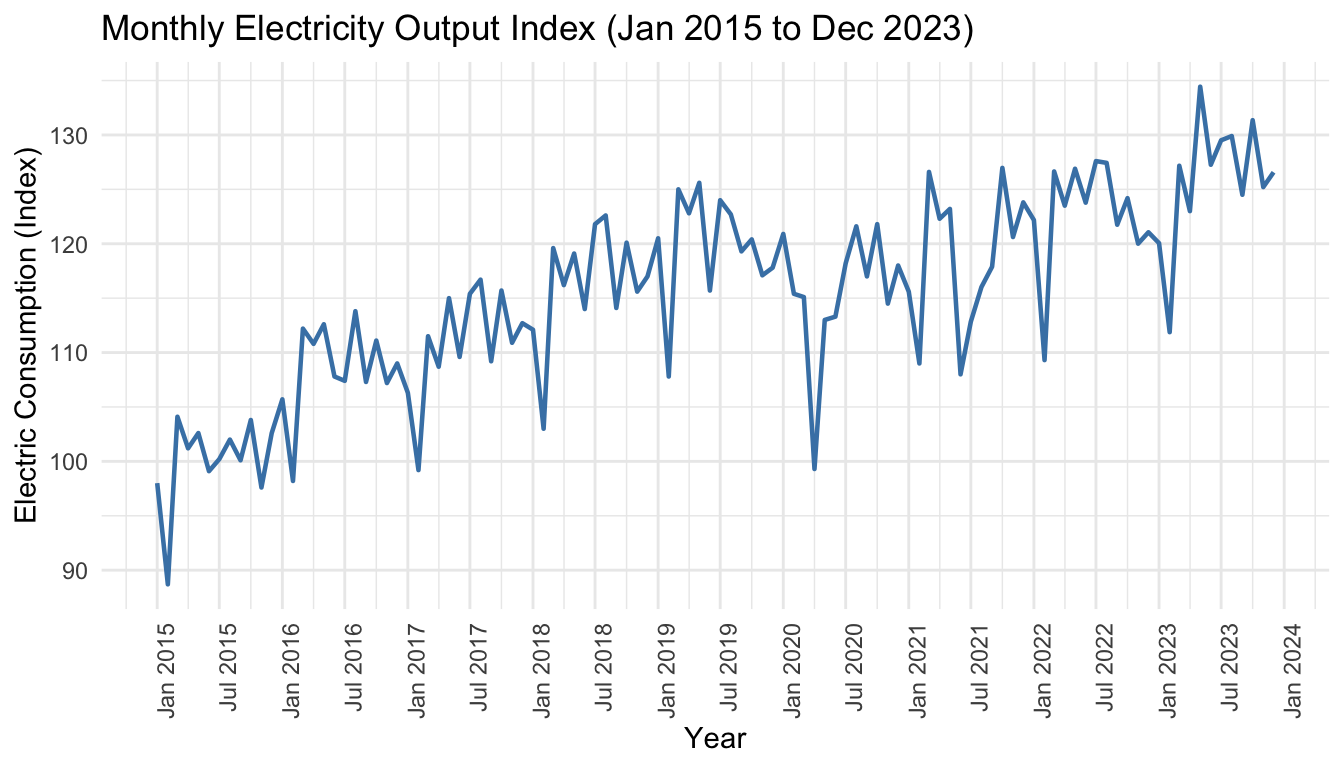

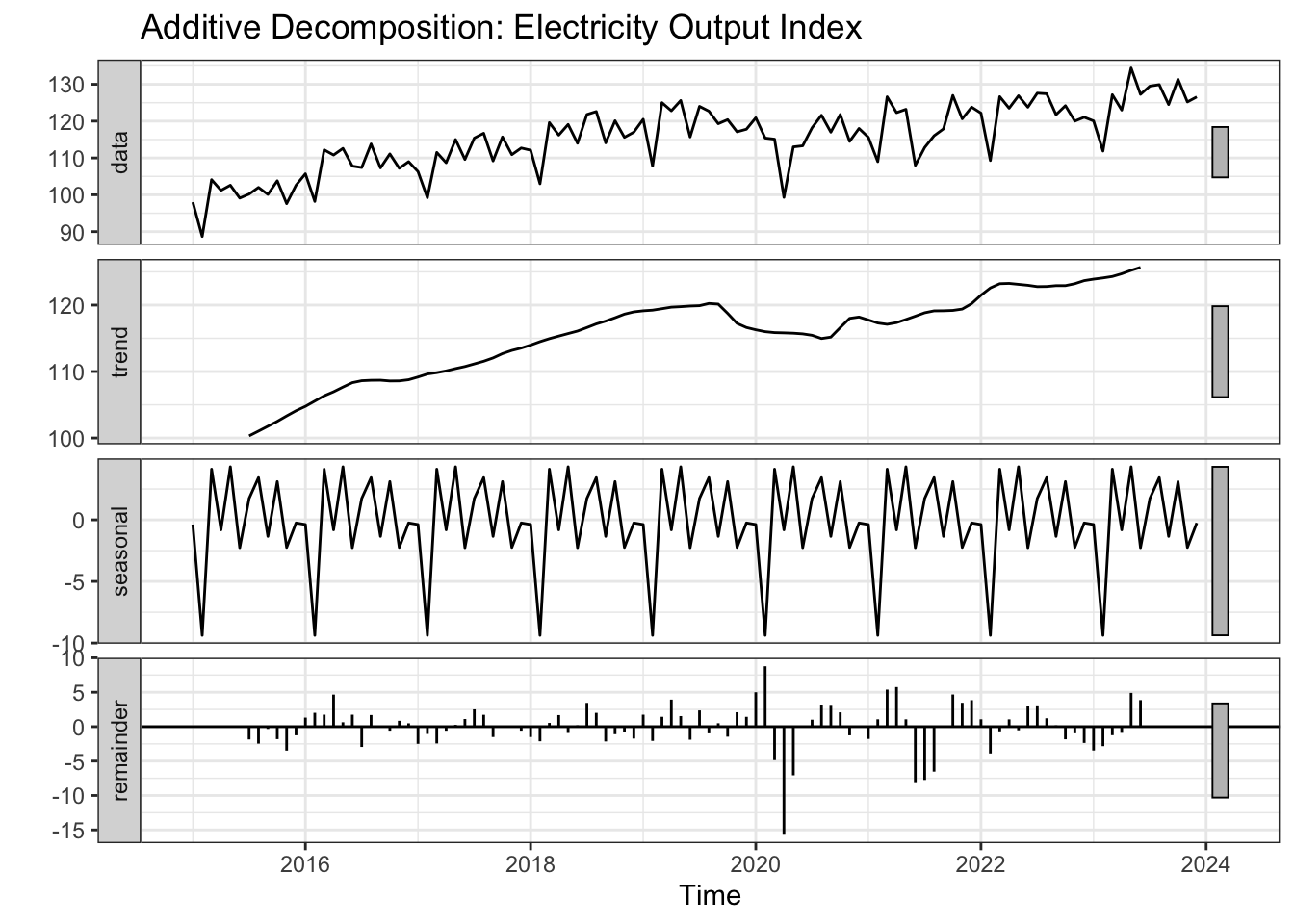

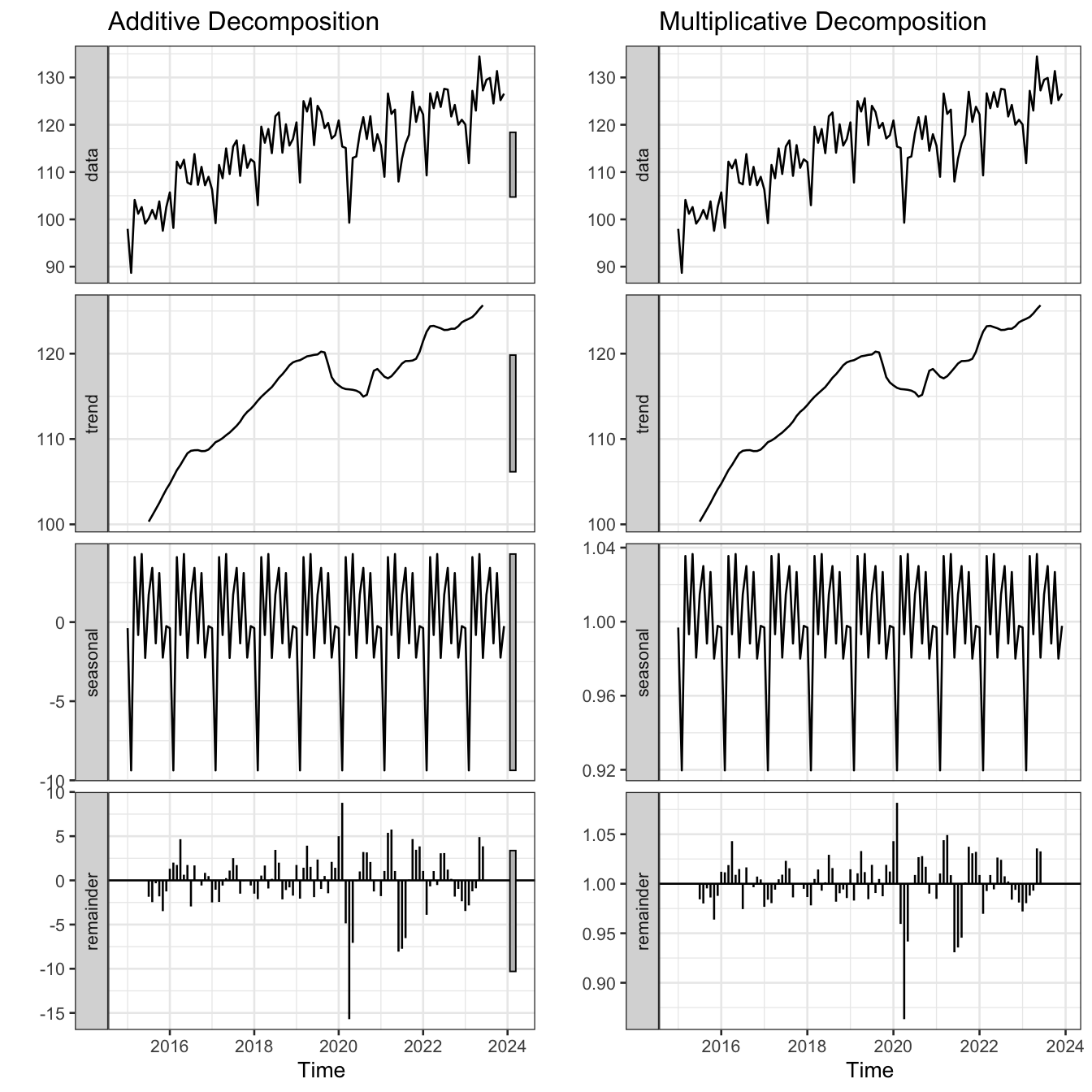

Figure 18: Additive vs. multiplicative decomposition of the electricity output index

Feature

Additive

Multiplicative

Seasonal magnitude

Constant

Grows with level

Use when

Seasonal swings roughly constant

Seasonal swings widen as series grows

Linearisation

Not needed

Apply log transform

R function

decompose(ts, type = "additive")

decompose(ts, type = "multiplicative")

Tip

If seasonal fluctuations grow proportionally with the level of the series → use multiplicative. If they remain roughly constant → use additive.

3.3.1 Examples

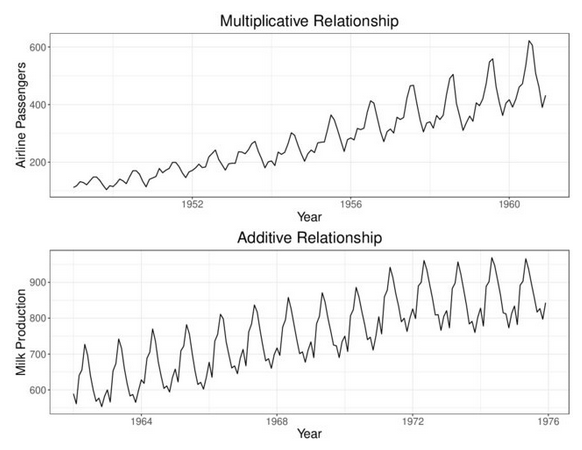

(a) Example 1 — Airline passengers (top): seasonal swings widen as the series grows → multiplicative. Milk production (bottom): seasonal swings remain roughly constant → additive.

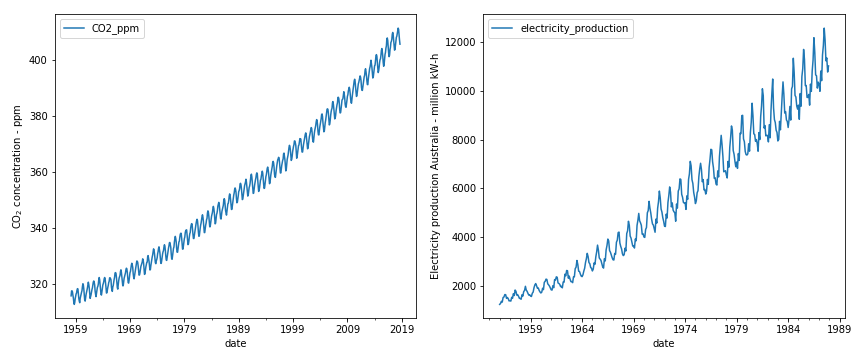

(b) Example 2 — CO₂ concentration (left) and Australian electricity production (right): both exhibit seasonal fluctuations that grow proportionally with the level → multiplicative.

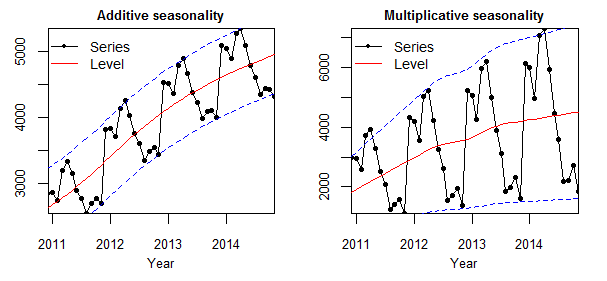

(c) Example 3 — Additive seasonality (left): the band of variation around the trend (dashed lines) stays constant. Multiplicative seasonality (right): the band widens as the level rises.

Figure 19: Real-world examples illustrating additive and multiplicative seasonal patterns.

4 Measuring Performance

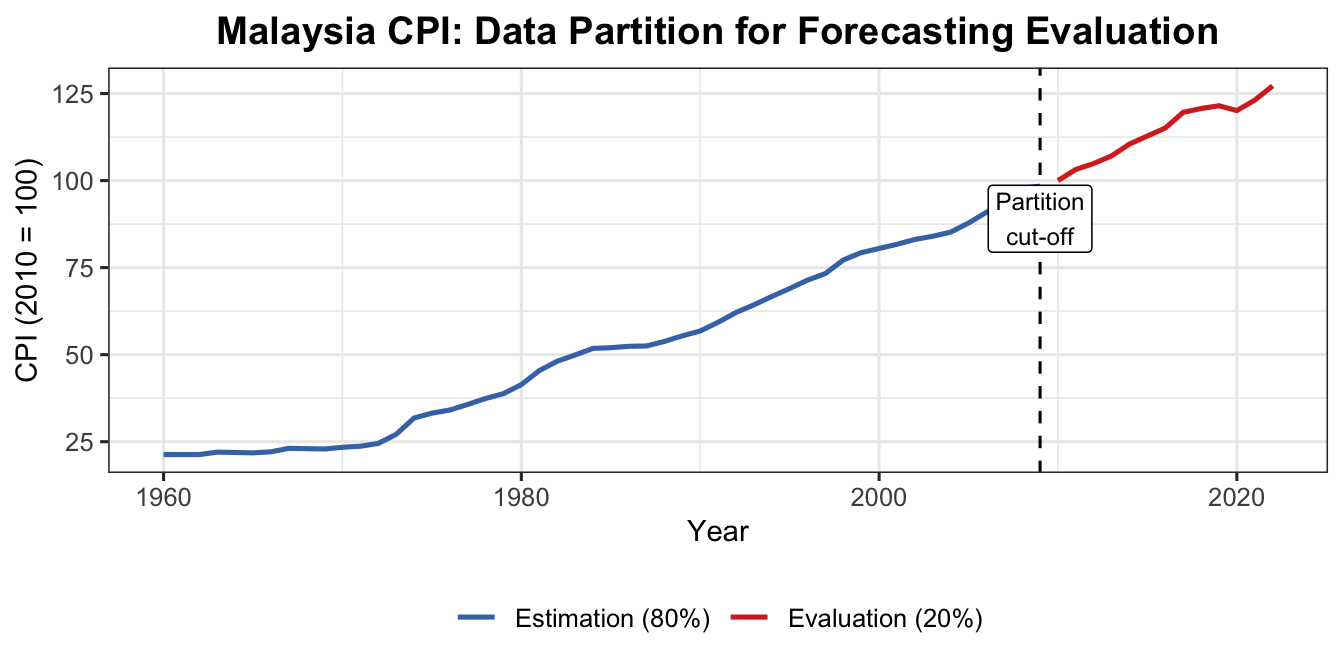

4.1 Data Partition

Part

Purpose

Rule of Thumb

Estimation (Training)

Fit the forecasting model

80% of data

Evaluation (Test)

Assess forecast accuracy

20% of data

Show R Code

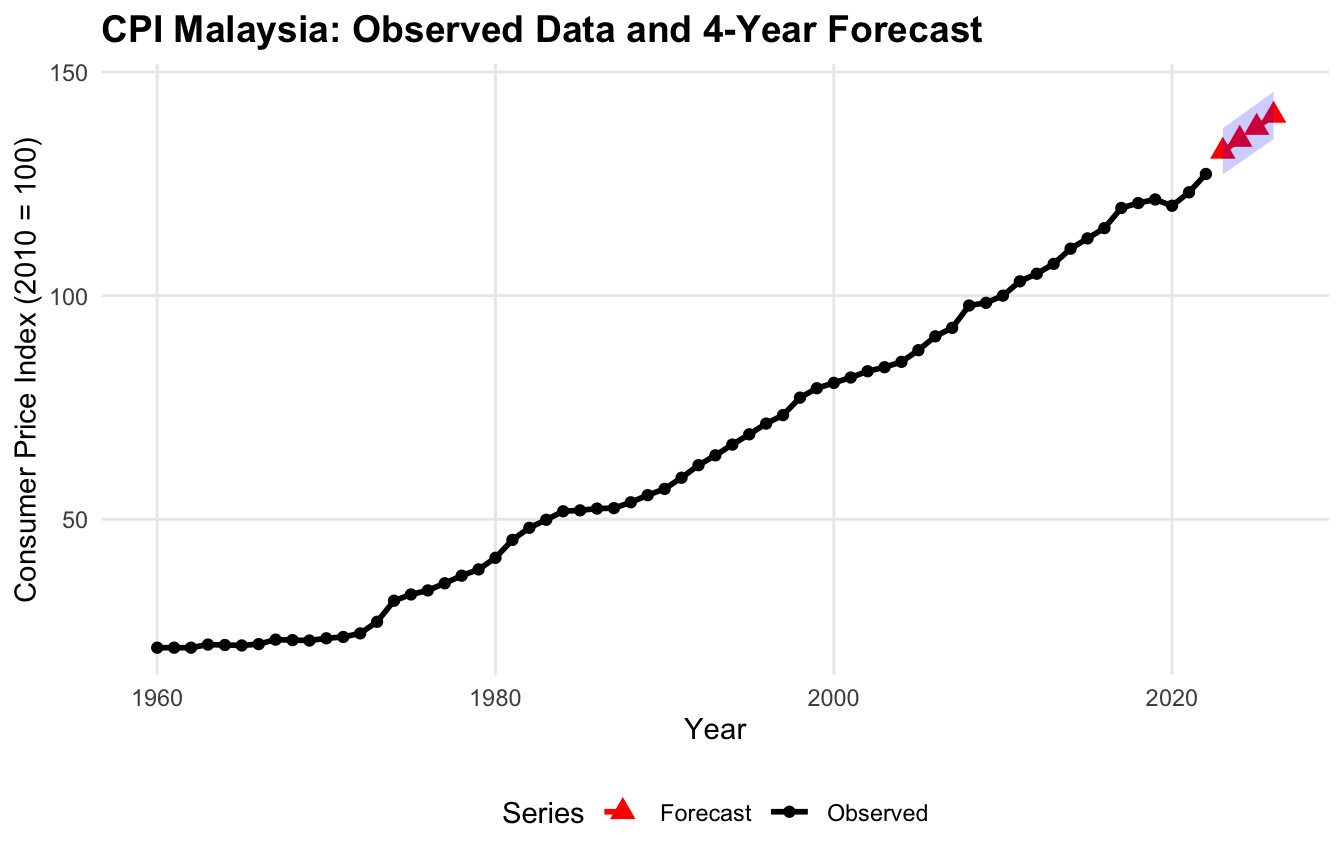

cpi <-read.csv("data/CPI Malaysia.csv", check.names =FALSE)cpits <-ts(cpi$`Consumer price index (2010 = 100)`,start =1960, frequency =1)est_part <-head(cpits, 0.8*length(cpits))eva_part <-tail(cpits, 0.2*length(cpits))str(est_part)

Time-Series [1:50] from 1960 to 2009: 21.3 21.3 21.3 22 21.9 21.8 22.1 23.1 23 22.9 ...

Show R Code

str(eva_part)

Time-Series [1:13] from 2010 to 2022: 100 103 105 107 110 ...

Robust to outliers; in original units; easy to compute

Disadvantage

Treats all forecast errors equally regardless of magnitude

Note

The best model produces the lowest error measure value.

A truly good model gives consistently low values across multiple error measures.

4.3 Example: Malaysia CPI Data

4.3.1 Model 1 — Linear Trend

Show R Code

n <-length(cpits)n_train <-length(est_part) # derived from actual 80% splitn_test <- n - n_traintime_train <-1:n_traintime_test <- (n_train +1):nmodel1 <-lm(est_part ~ time_train)summary(model1)

Call:

lm(formula = est_part ~ time_train)

Residuals:

Min 1Q Median 3Q Max

-6.2836 -3.3028 -0.2493 2.3069 10.7824

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 8.82882 1.11813 7.896 3.16e-10 ***

time_train 1.68883 0.03816 44.255 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 3.894 on 48 degrees of freedom

Multiple R-squared: 0.9761, Adjusted R-squared: 0.9756

F-statistic: 1959 on 1 and 48 DF, p-value: < 2.2e-16